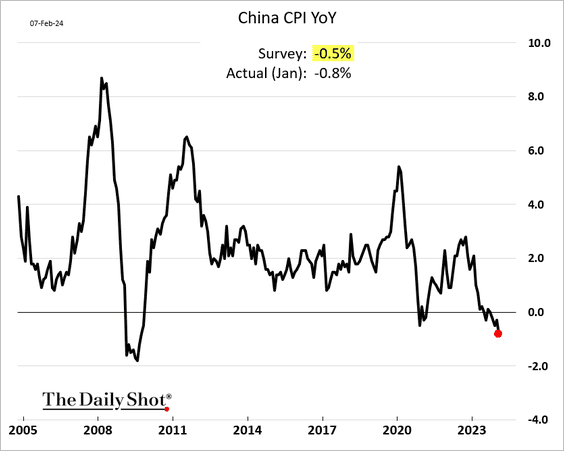

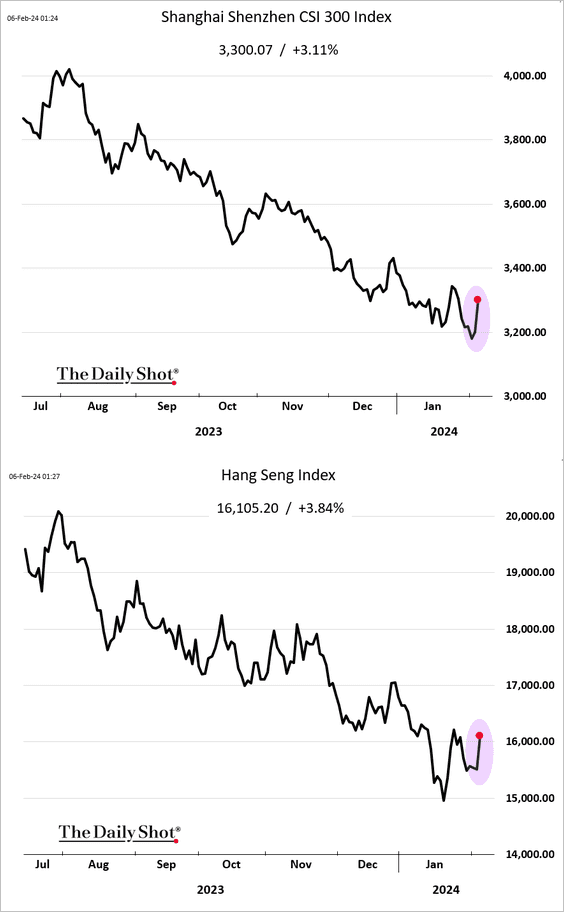

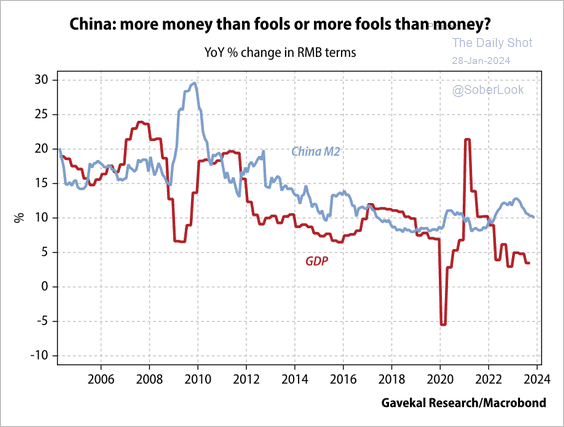

China: China’s disinflationary pressures persist, partly reflecting weak domestic demand. In January, the CPI had its biggest year-over-year decline since the GFC.

Source: The Daily ShotSource: South China Morning Post Read full article

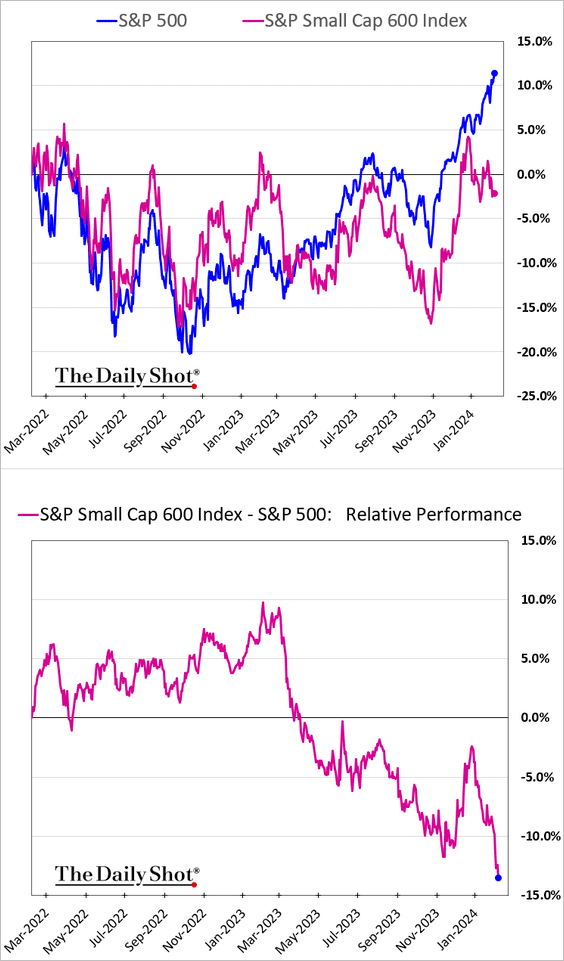

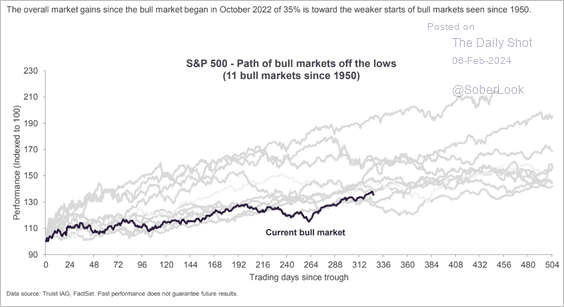

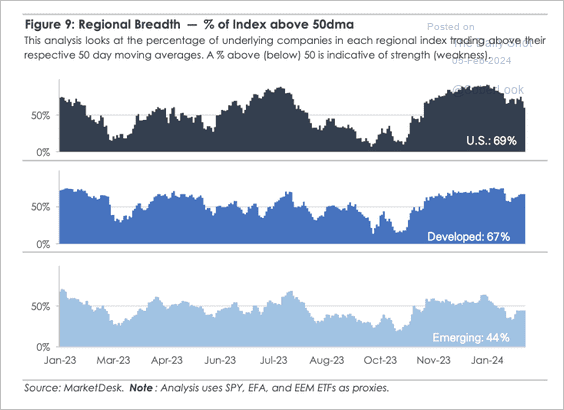

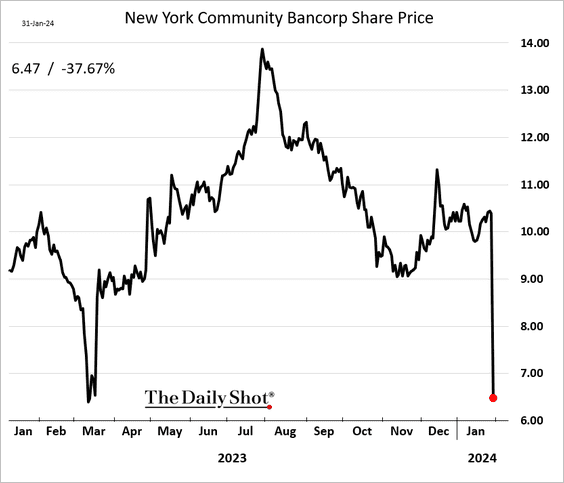

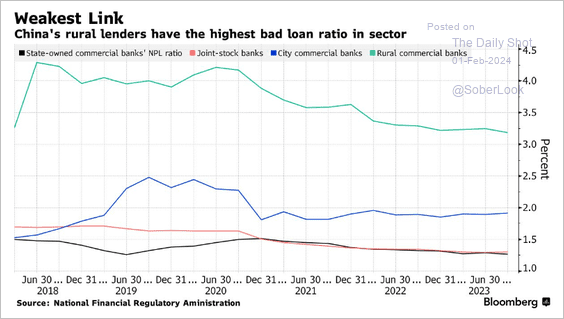

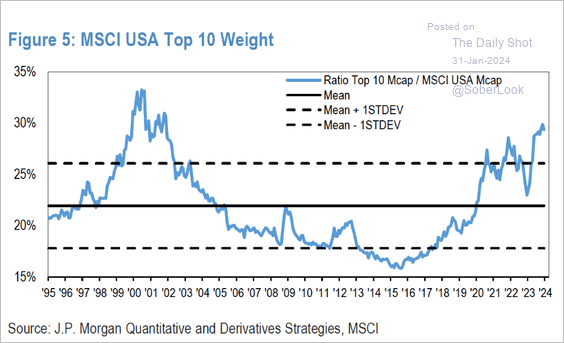

Equities: Small-cap underperformance widened in recent days, exacerbated by pressure on smaller banks.

Source: The Daily Shot

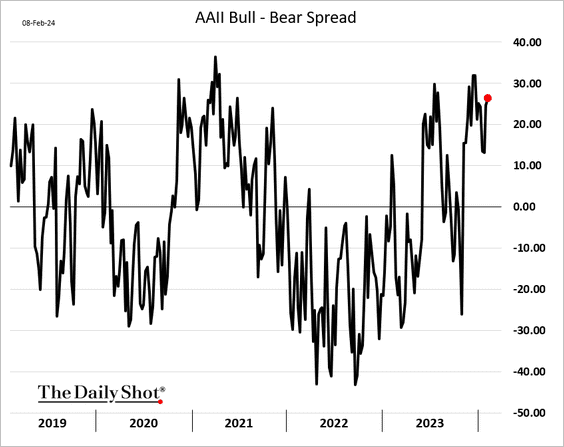

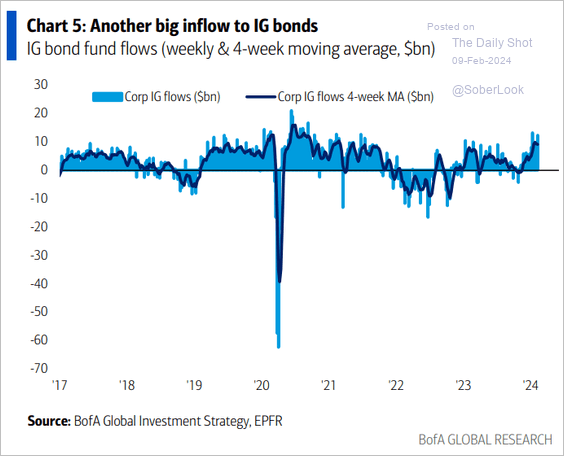

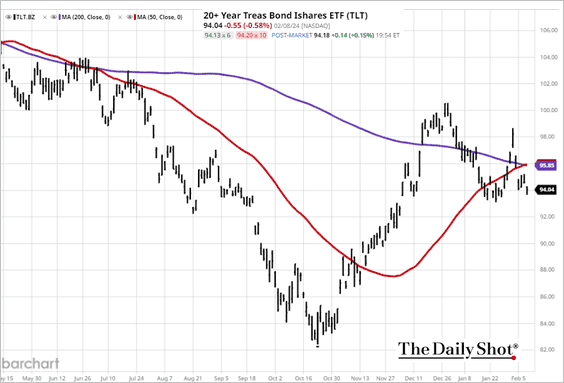

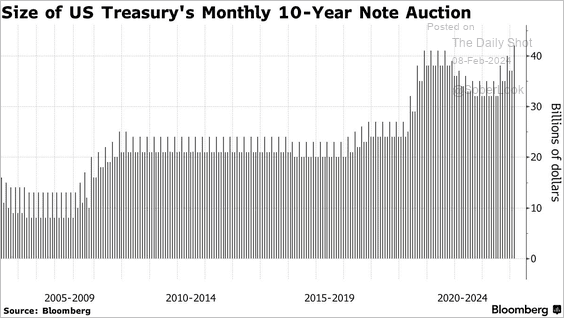

Rates: A record-high 10-year note auction was met with solid demand on Wednesday, sending yields lower.

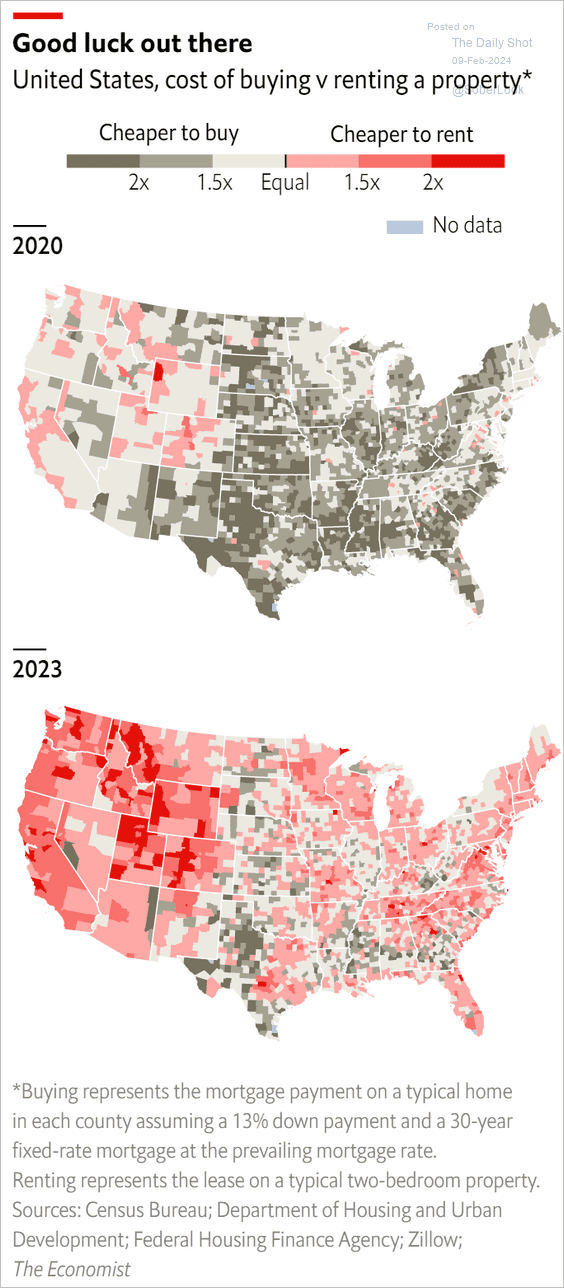

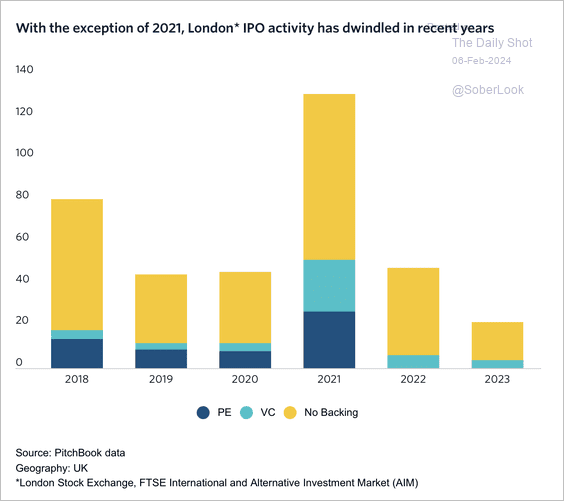

The United Kingdom: London’s IPO activity has weakened over the past two years as more British companies decided to list in New York or elsewhere in Europe.

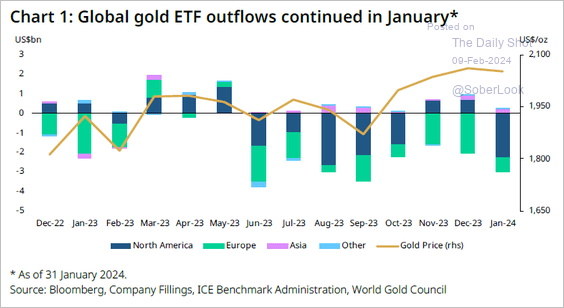

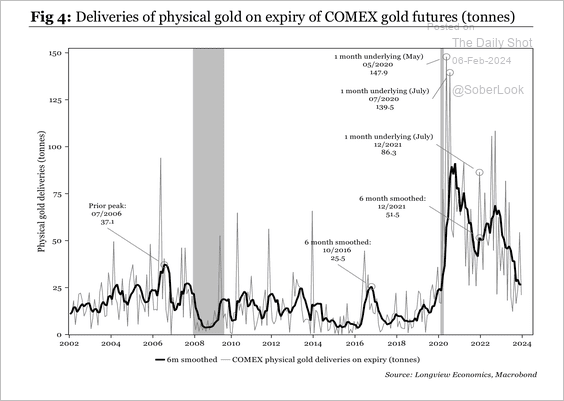

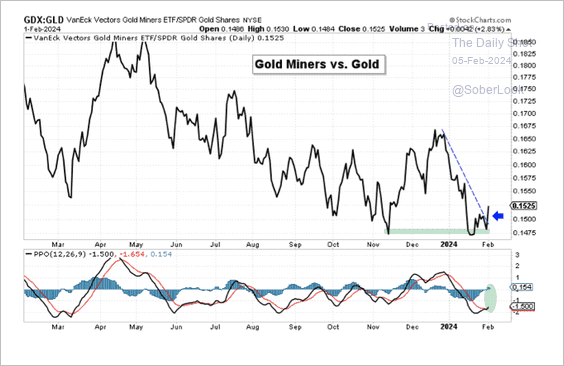

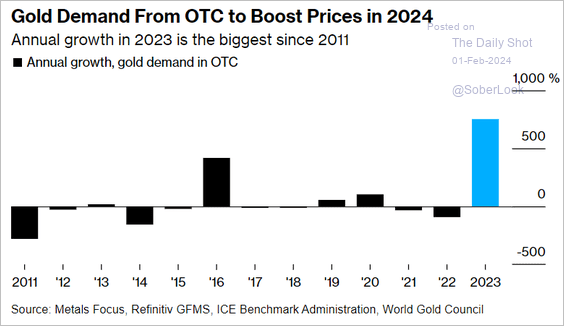

Commodities: Physical gold deliveries have trended lower in recent years, possibly because investors and governments have chosen to hoard gold as geopolitical risks increased.

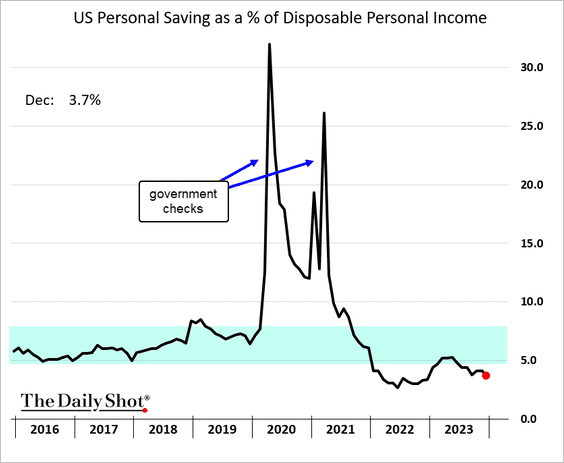

The United States: Consumers continue to save less than they did prior to the pandemic (relative to their disposable incomes). The rate has been trending lower since last spring.

Source: The Daily Shot

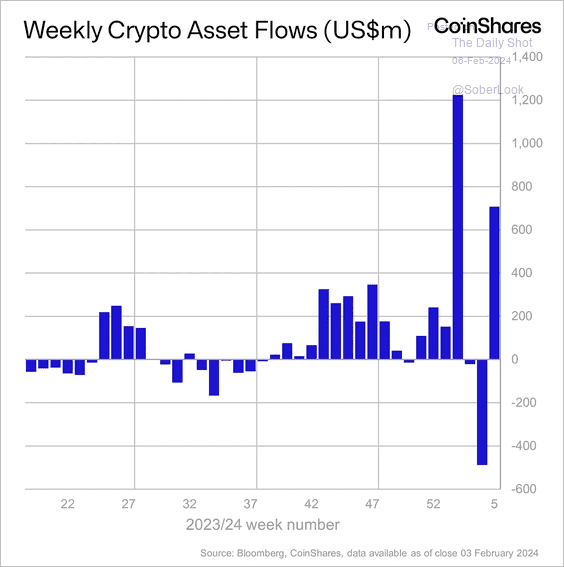

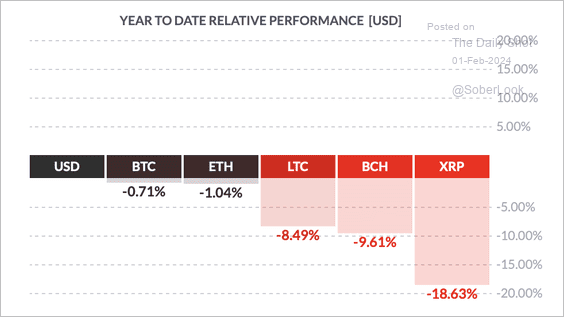

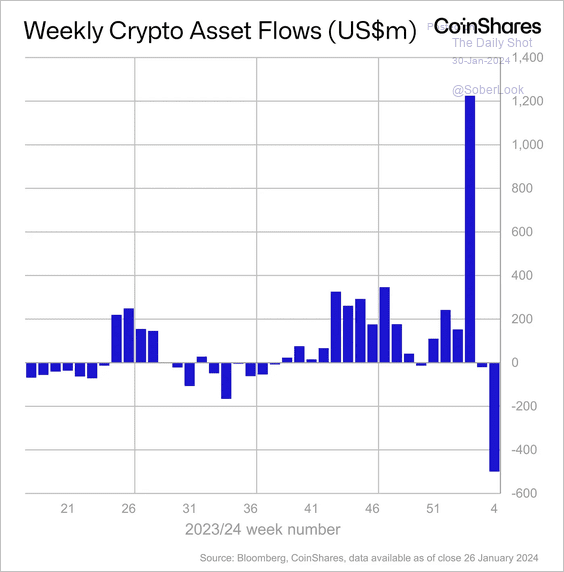

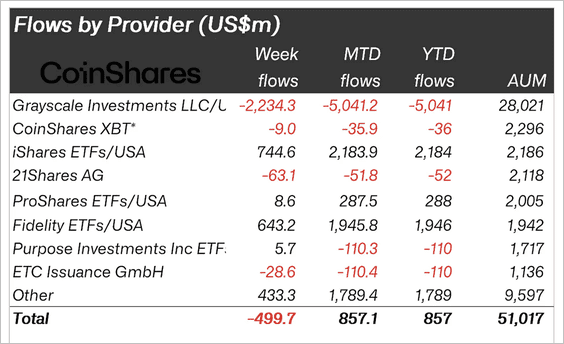

Cryptocurrency: Crypto funds saw significant outflows last week, mostly driven by incumbent bitcoin ETF issuer Grayscale.

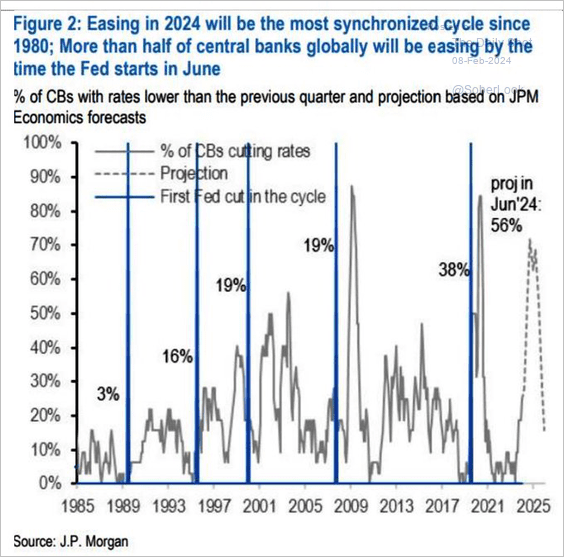

Rates: The average real Fed funds rate at the first rate cut is 3% (median 2.8%). In this cycle, the real rate could exceed the historical average if inflation continues to decline.