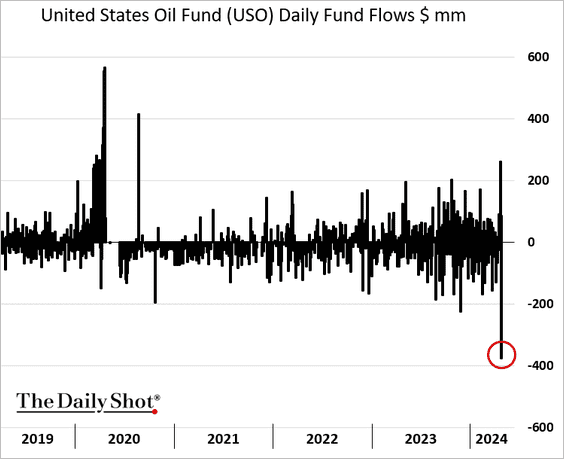

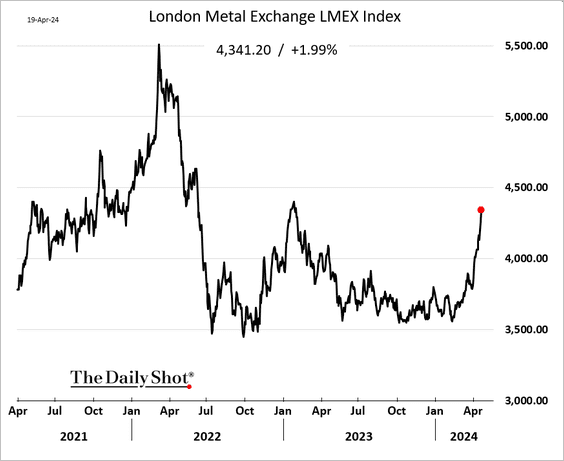

Commodities: Gold is trading at a premium on the Shanghai Exchange relative to the US-based Intercontinental Exchange (ICE), and ETF holdings have diverged between the two markets.

Momentum is currently exposed to strong economic growth and high interest rates. The risk of a momentum reversal should remain low in the absence of a significant macro shift or geopolitical shock, according to BlackRock.

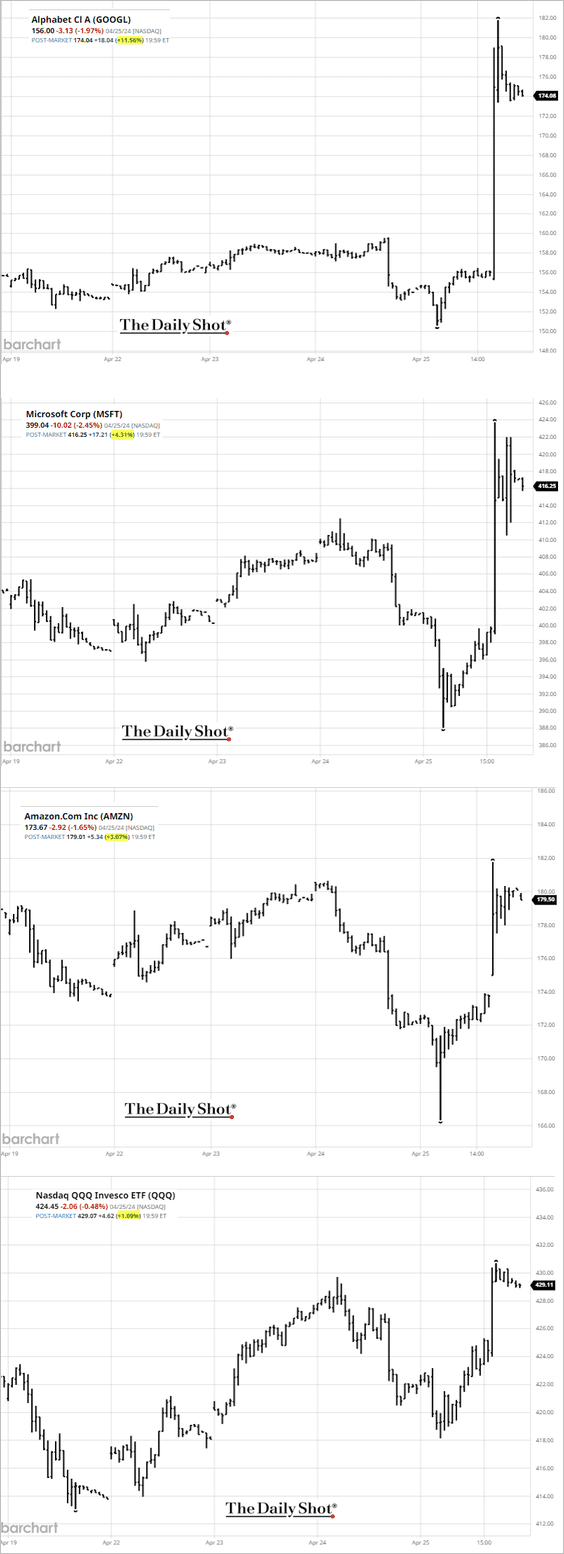

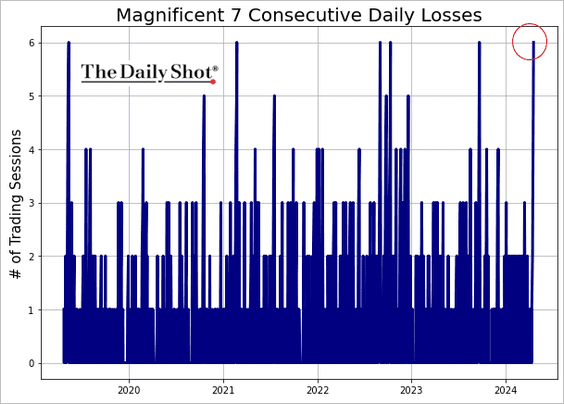

Equities: Shares of tech giants surged in after-hours trading as the market responded positively to announcements from Alphabet and other major players.

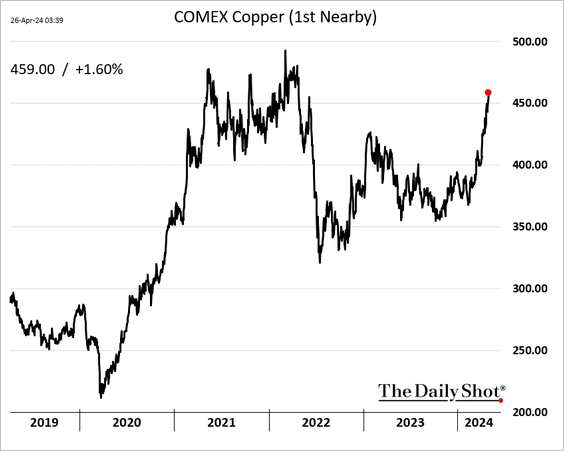

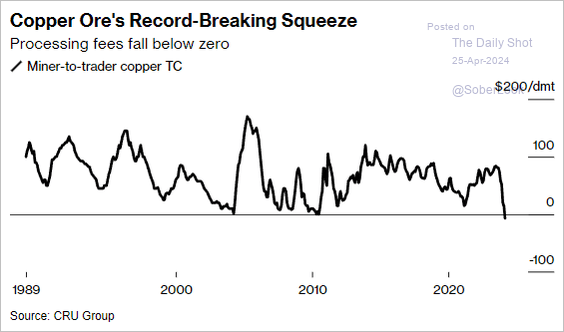

Commodities: The market for semi-processed copper ore is currently facing exceptional scarcity, as traders and smelters are paying prices for copper ore that nearly match its processed value, suggesting a lack of readily available supplies

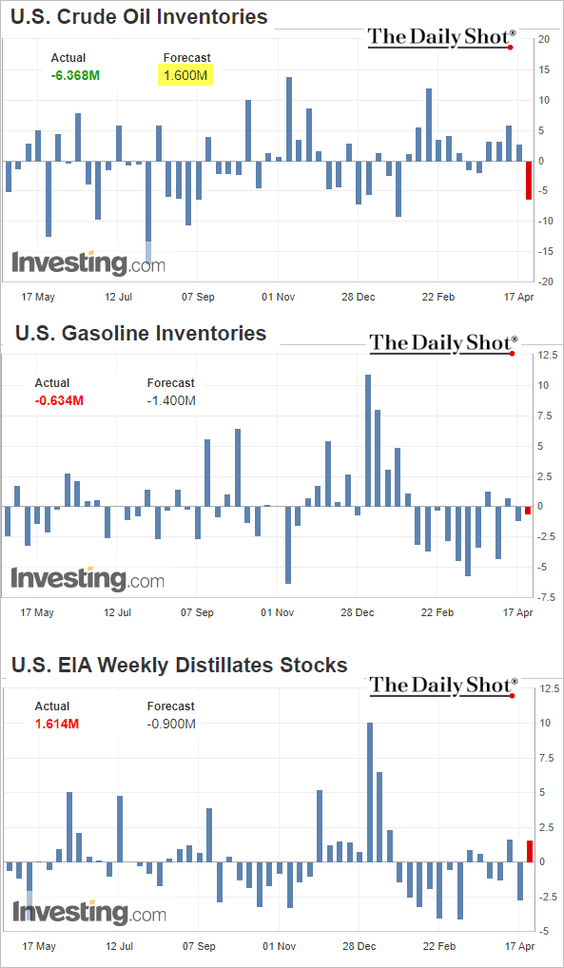

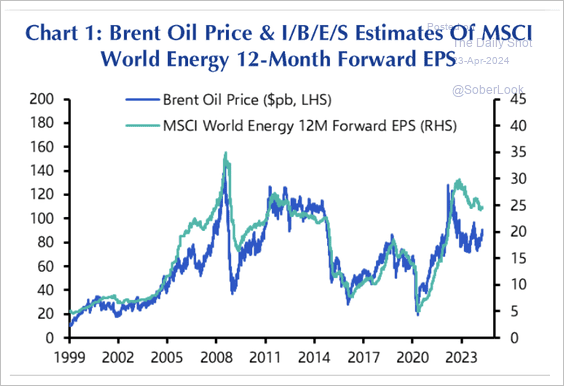

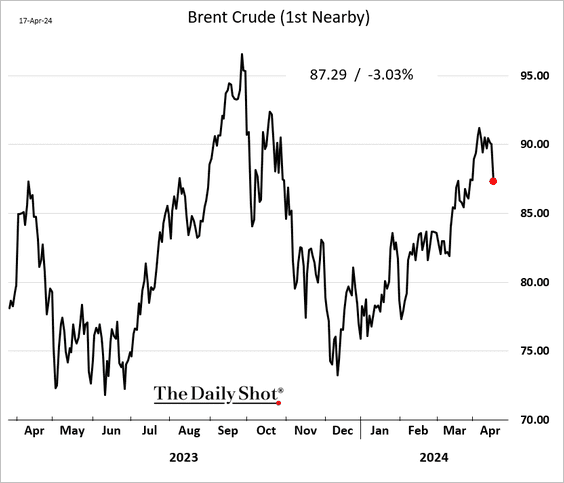

Energy: US crude oil stockpiles declined sharply last week (the market expected an increase). Inventory data for refined products was less bullish. Below are weekly changes.

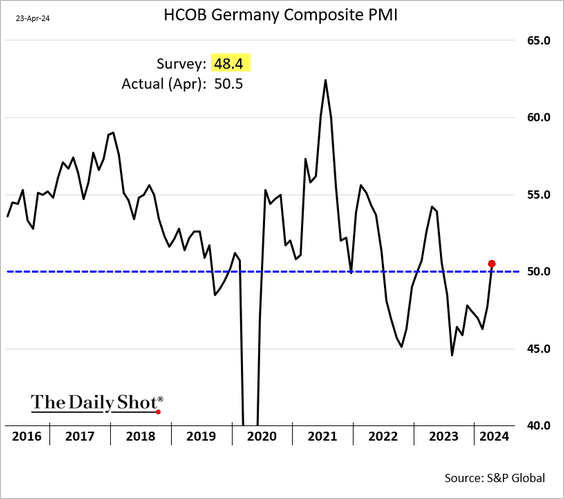

The Eurozone: Germany’s composite PMI is back in growth mode, topping expectations. The improvement was driven by services, with the manufacturing slump persisting this month.

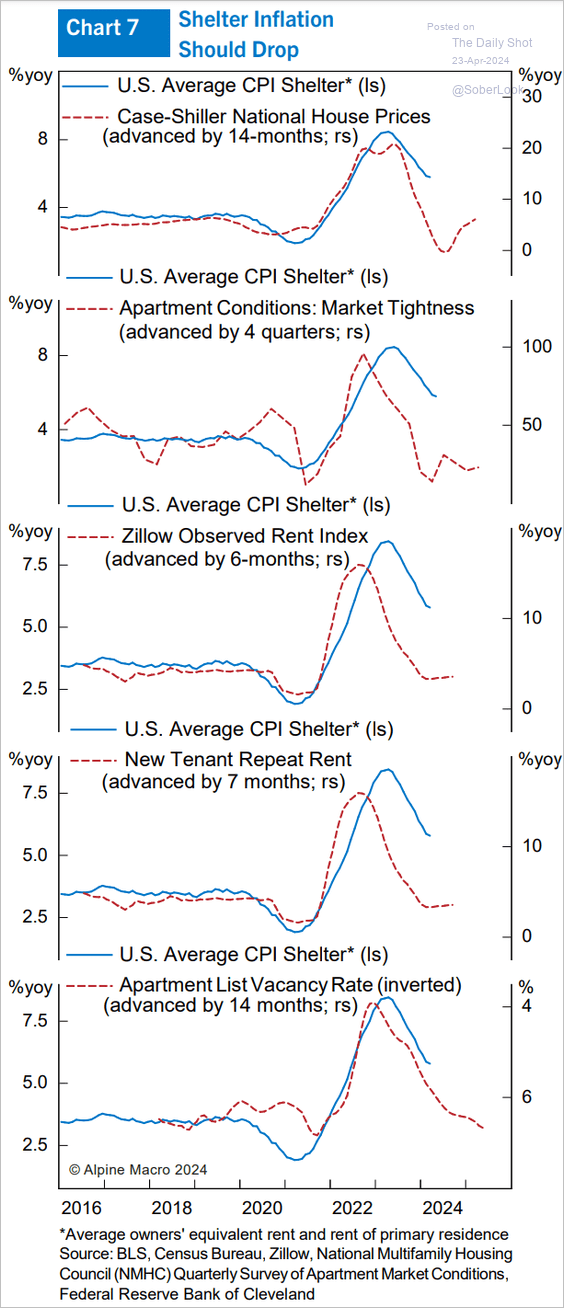

Source: The Daily Shot

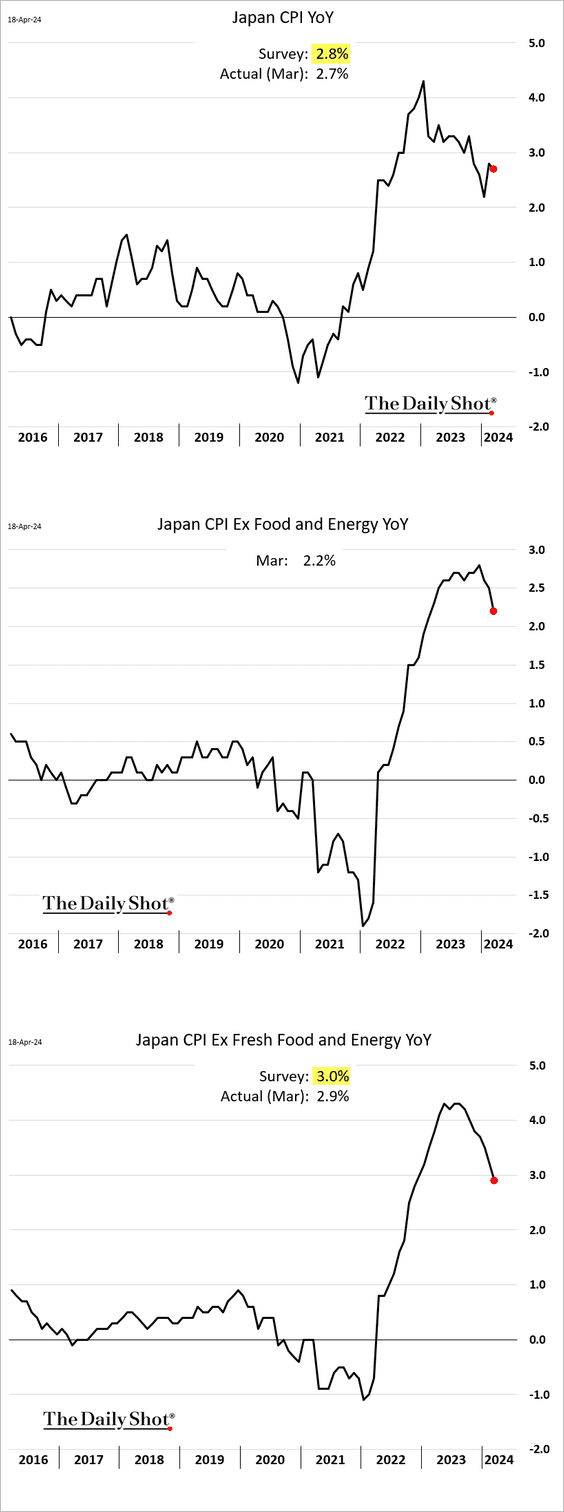

Japan: Services CPI could climb further, forcing the BoJ to deliver another rate hike.

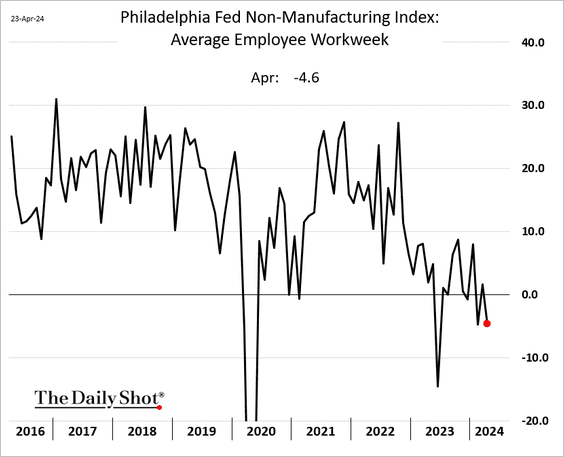

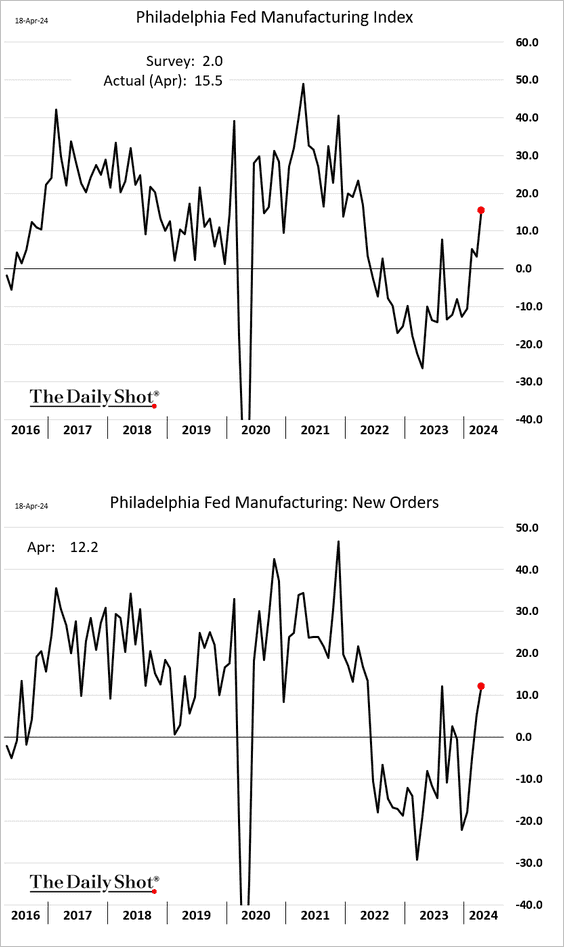

The United States: The Philly Fed’s regional manufacturing index rose this month, signaling an improvement in US factory activity. This report contrasts with the earlier data from the New York Fed.

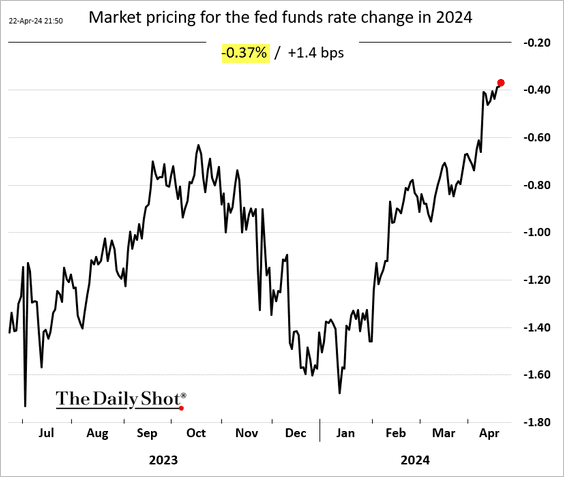

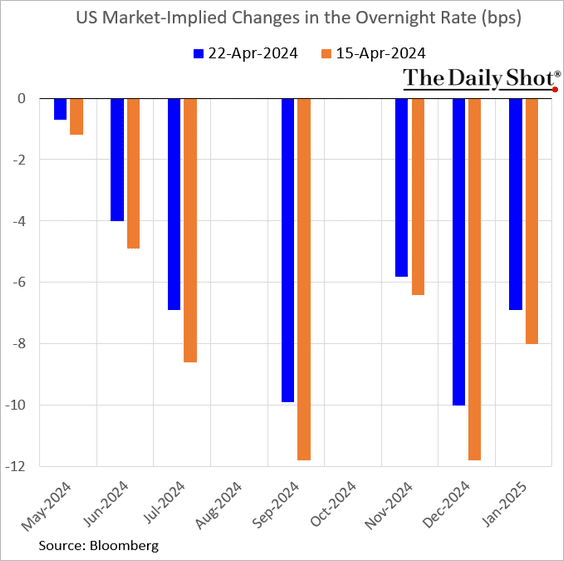

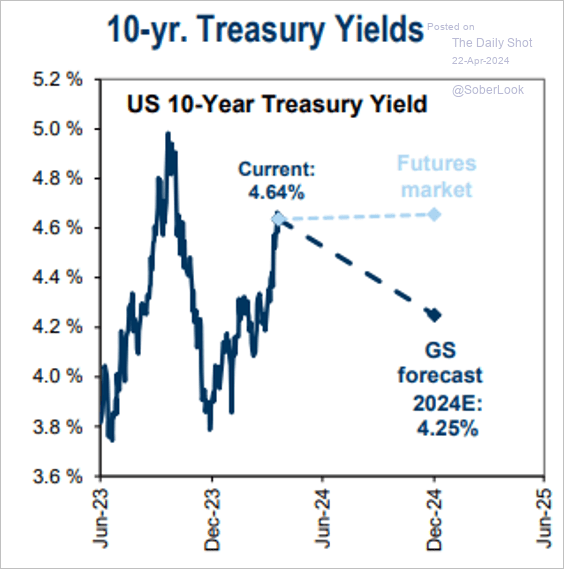

Rates: Some traders are betting that the economy and inflation will weaken significantly in the months ahead, forcing the Fed to deliver three rate cuts.

{kind=link}