Greetings,

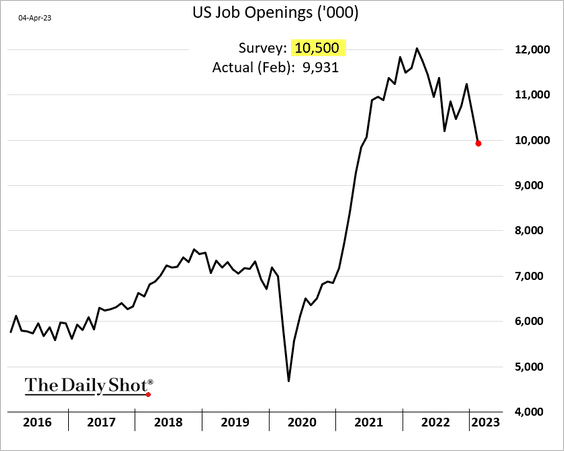

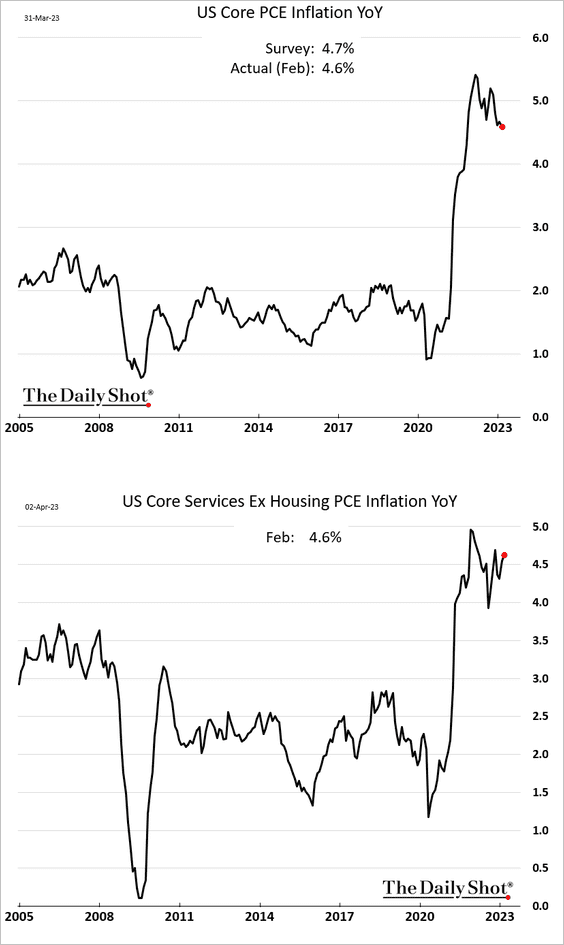

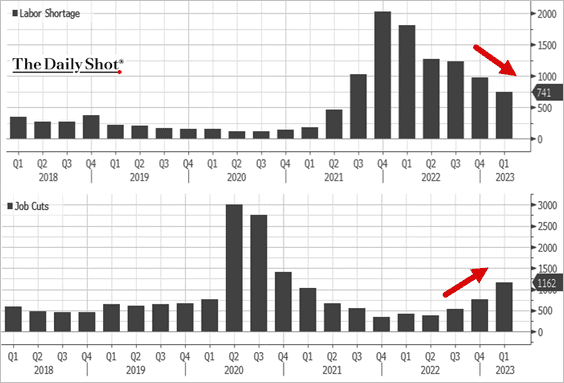

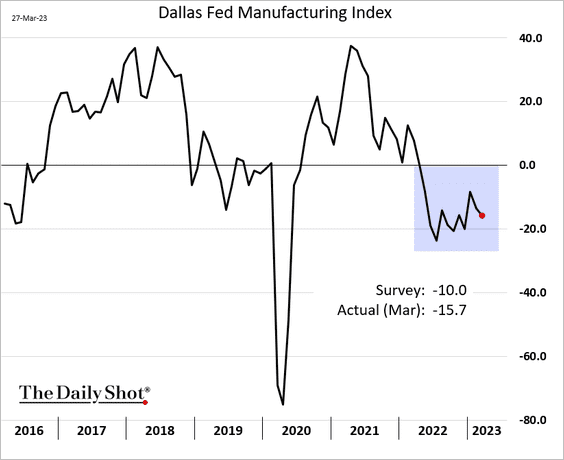

The United States: Job openings declined more than expected in February.

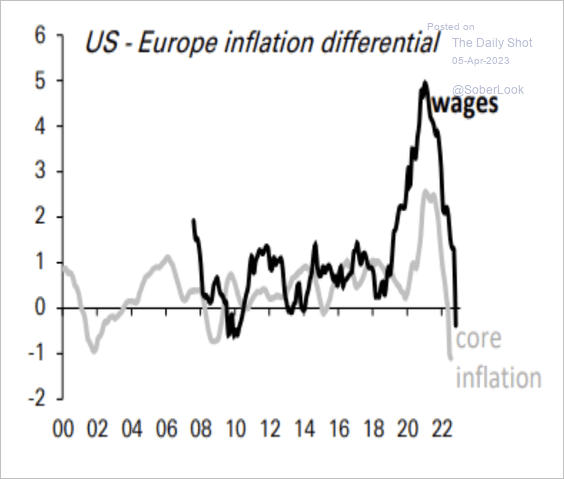

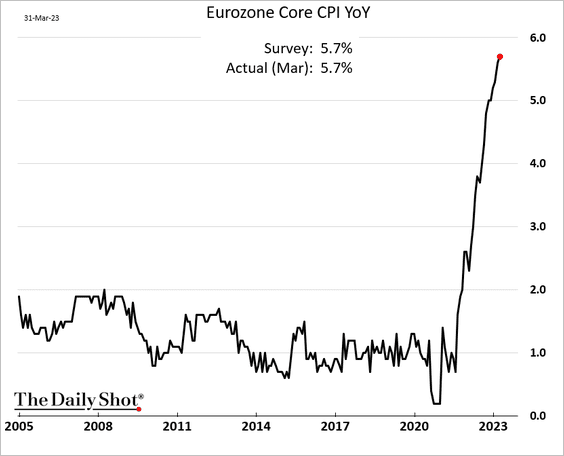

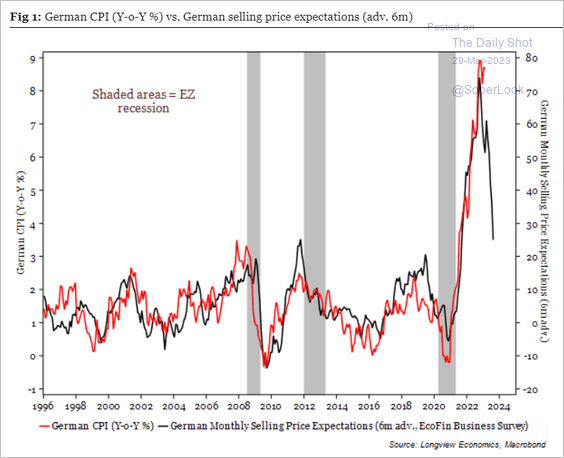

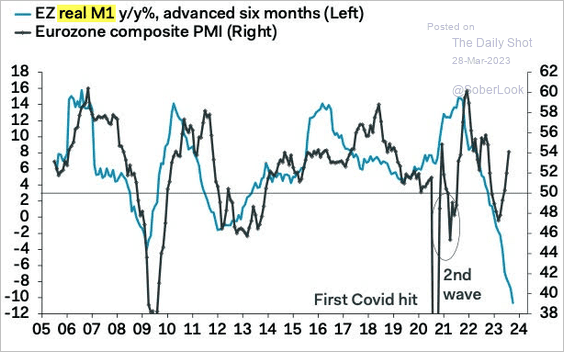

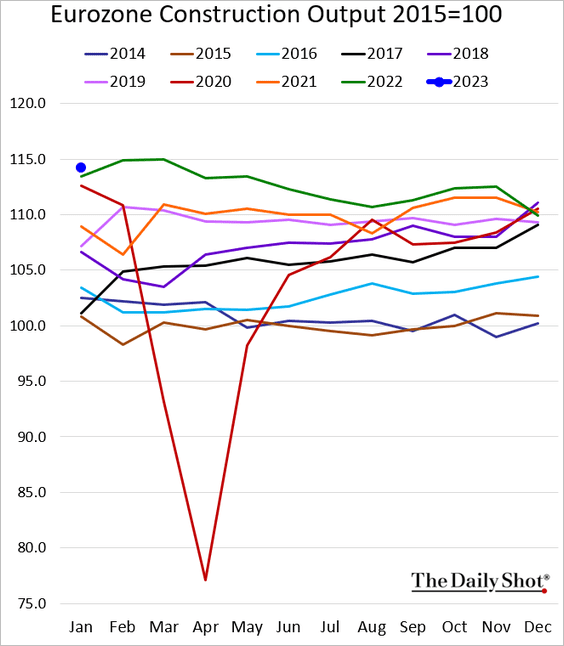

The Eurozone: Wage growth and CPI are now higher in the Eurozone versus the US.

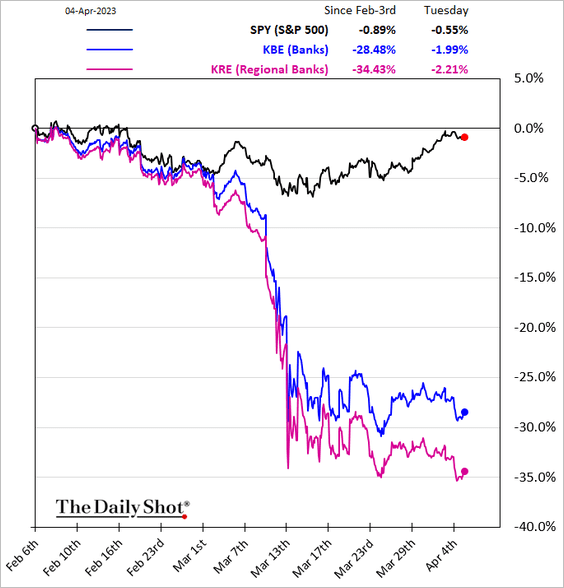

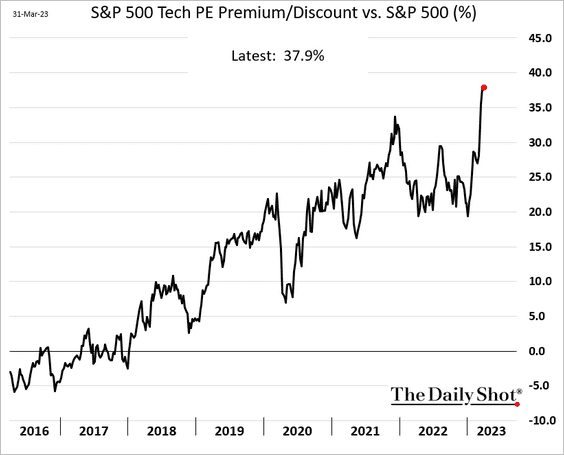

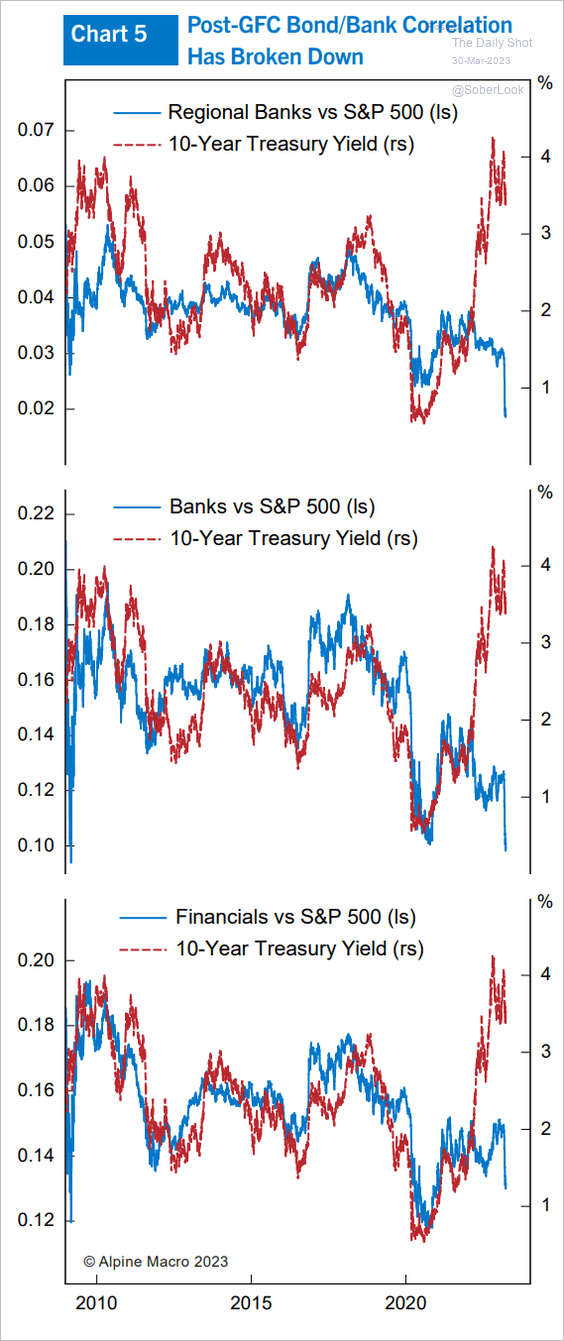

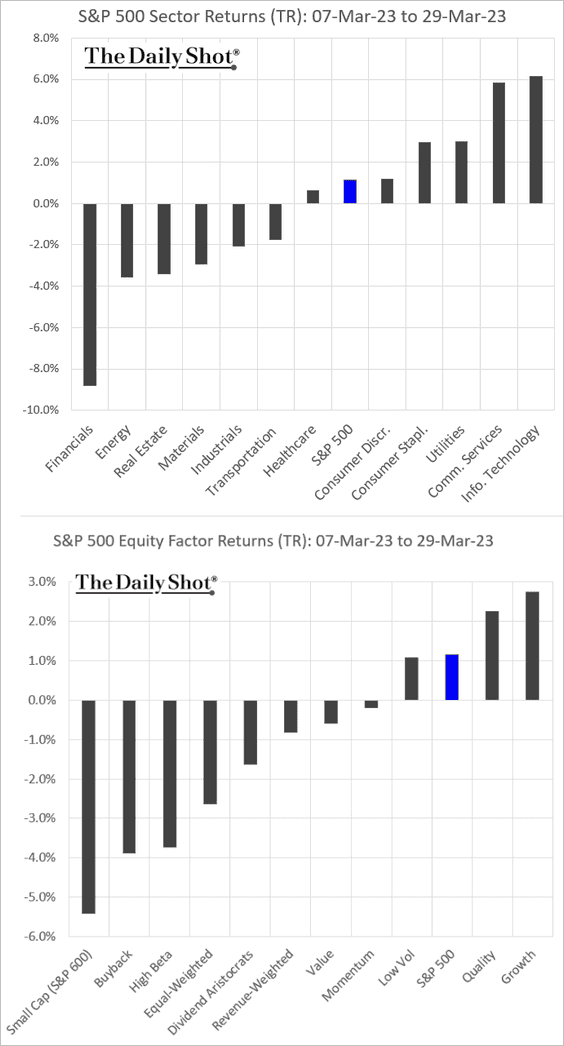

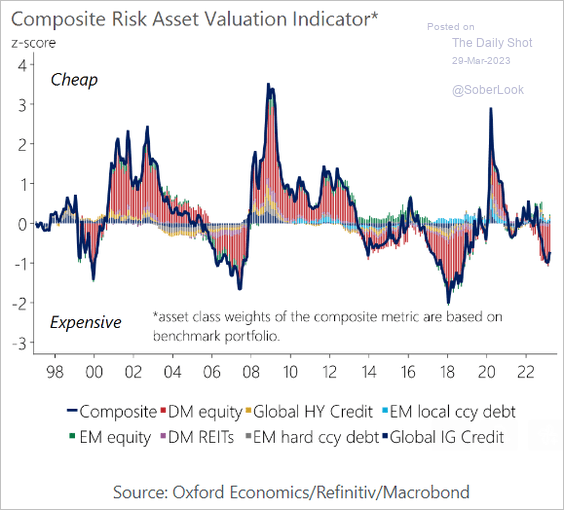

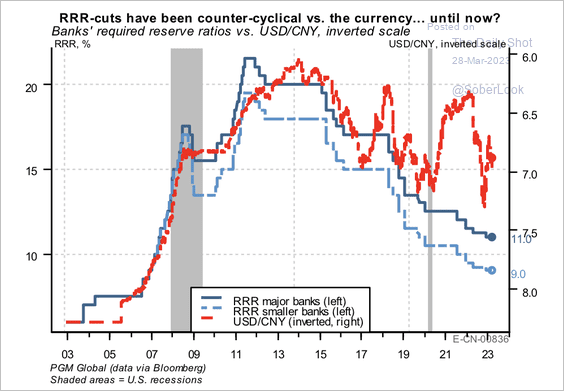

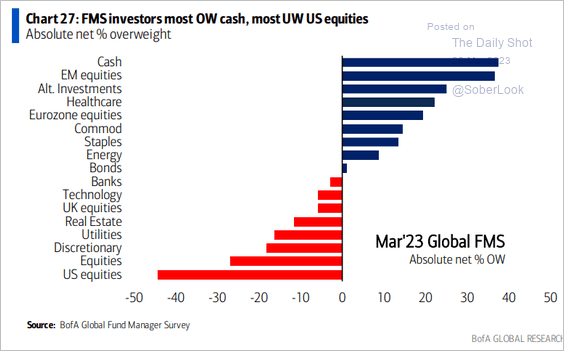

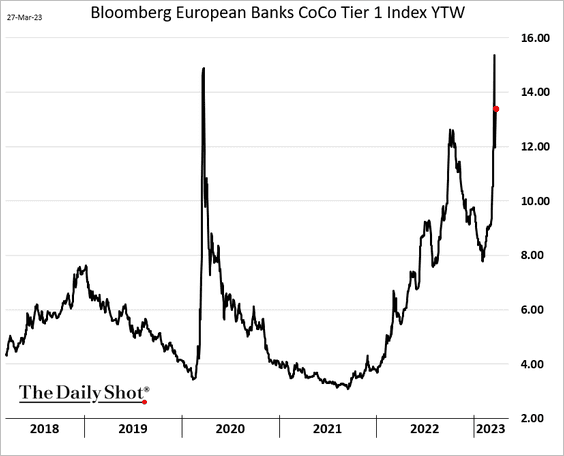

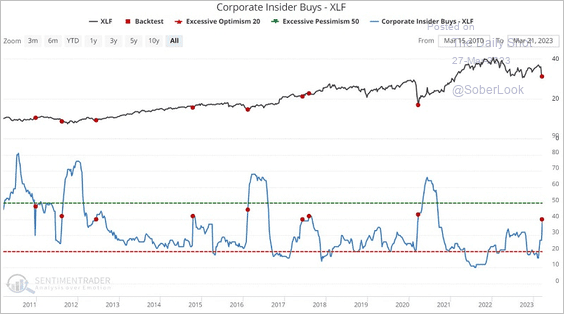

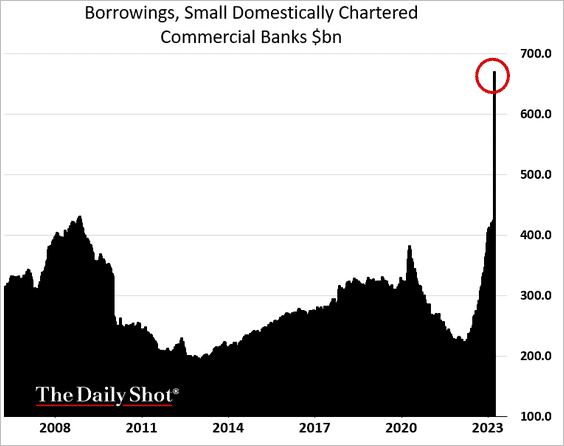

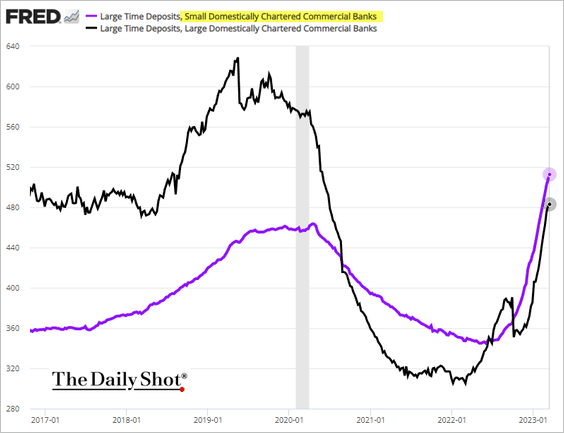

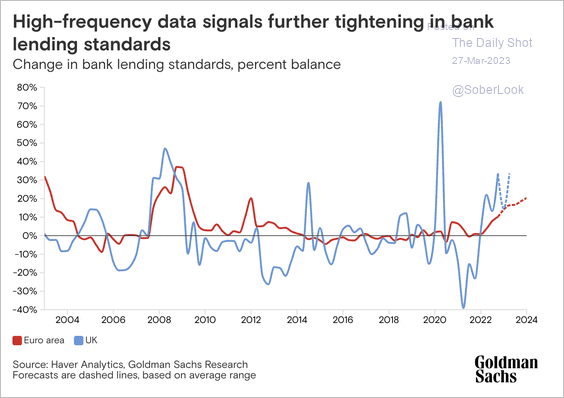

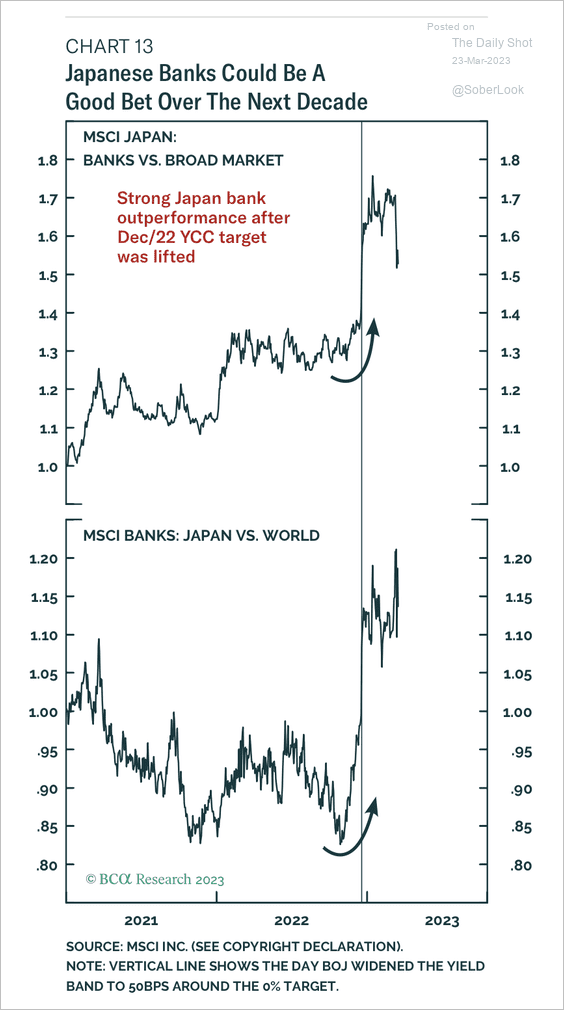

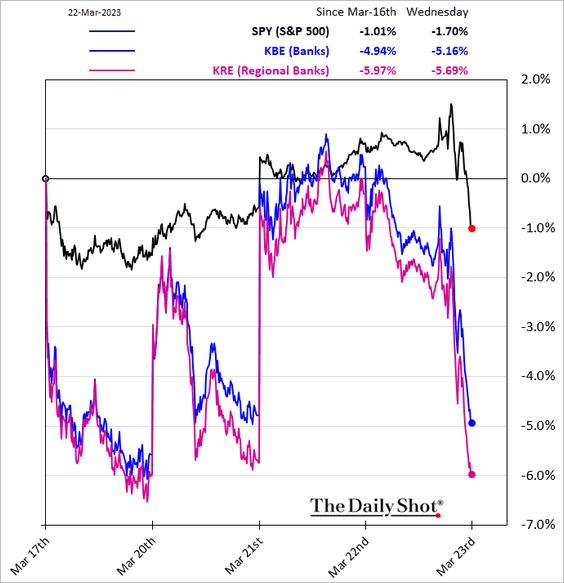

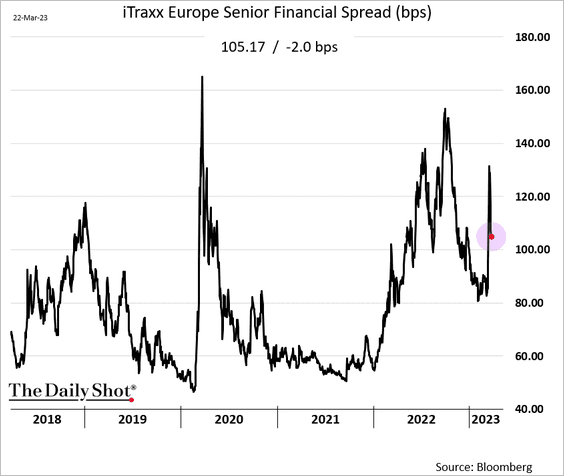

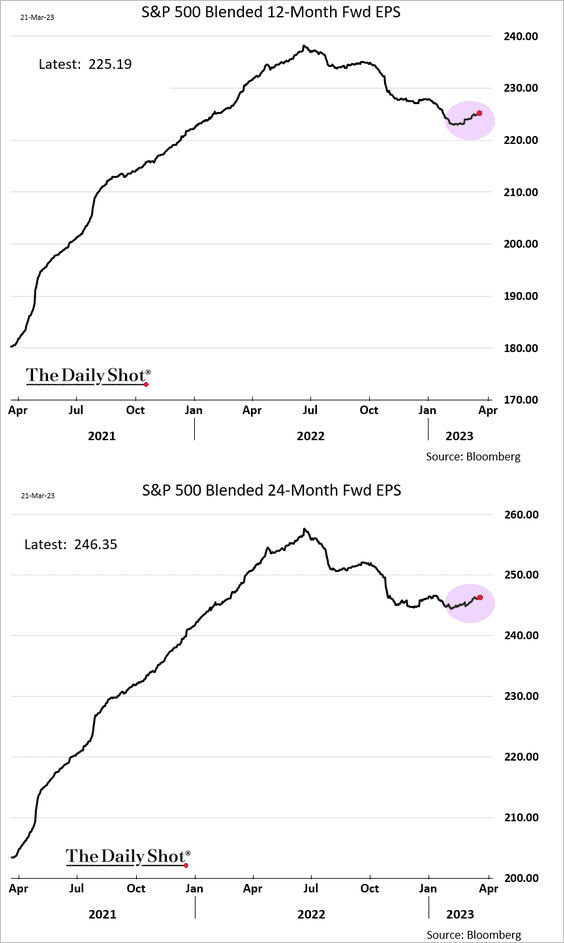

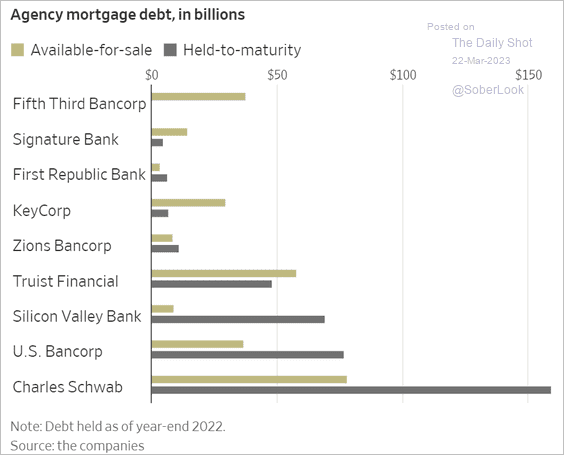

Equities: Bank shares continue to struggle.

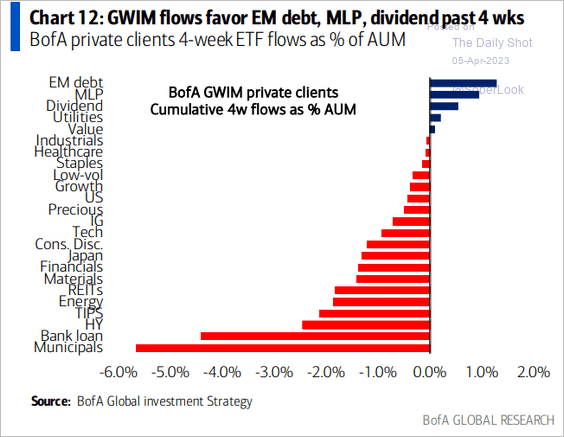

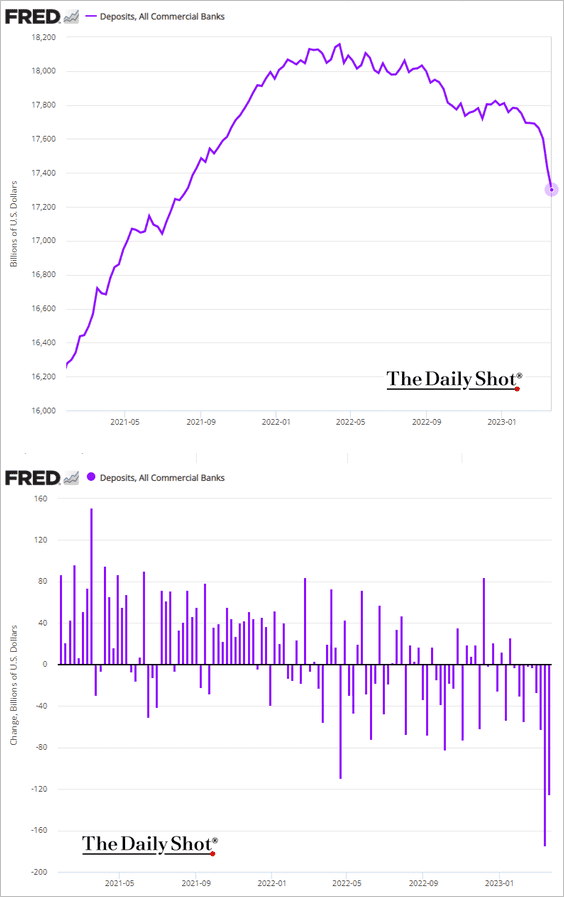

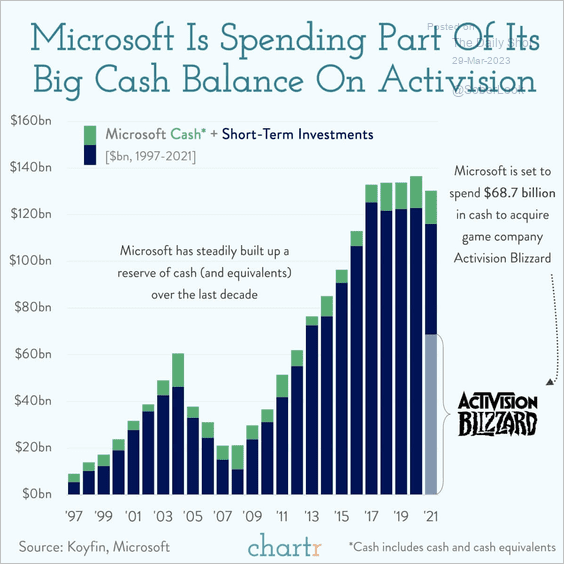

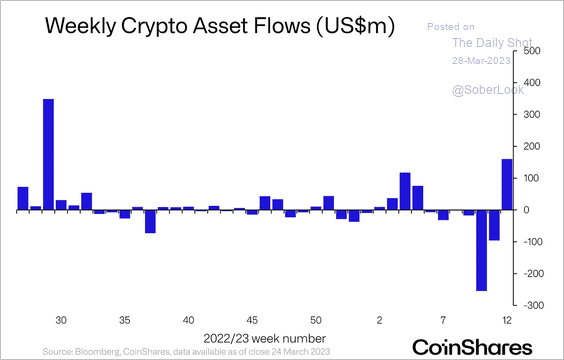

Credit: BofA’s private clients have also been getting out of munis.

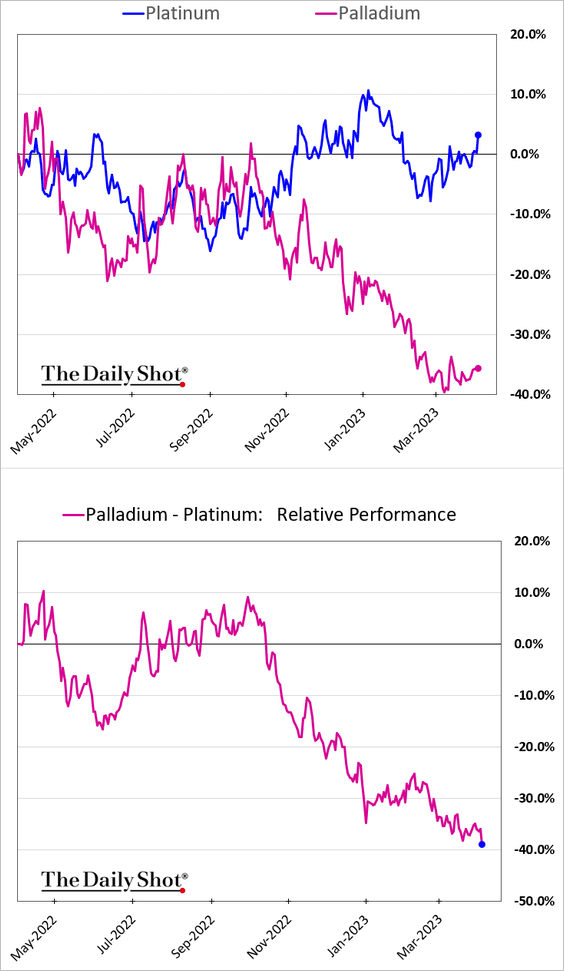

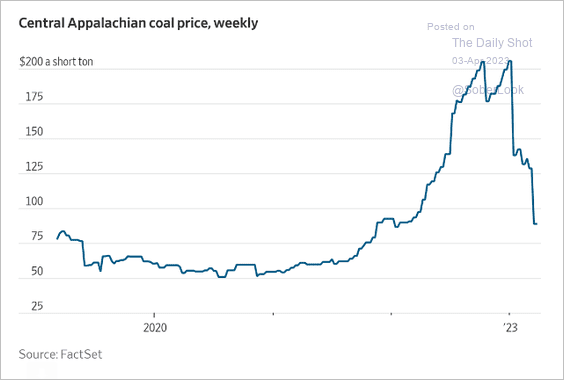

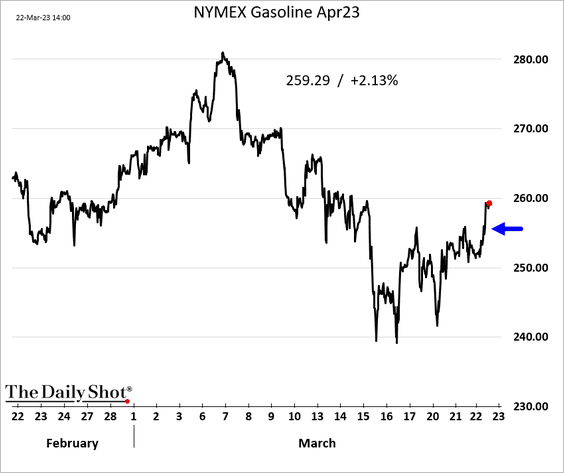

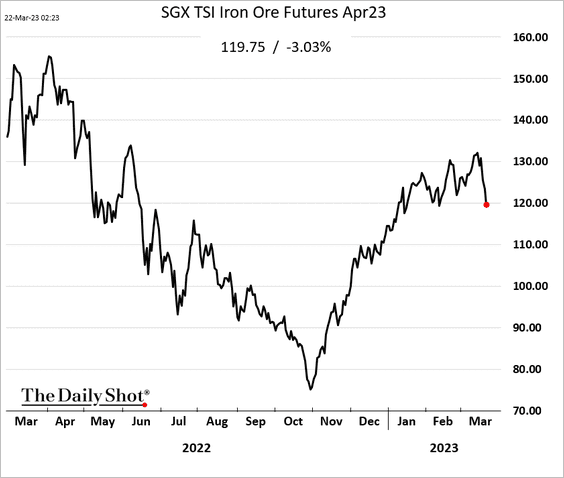

Commodities: Palladium’s underperformance widened further as platinum prices jumped.

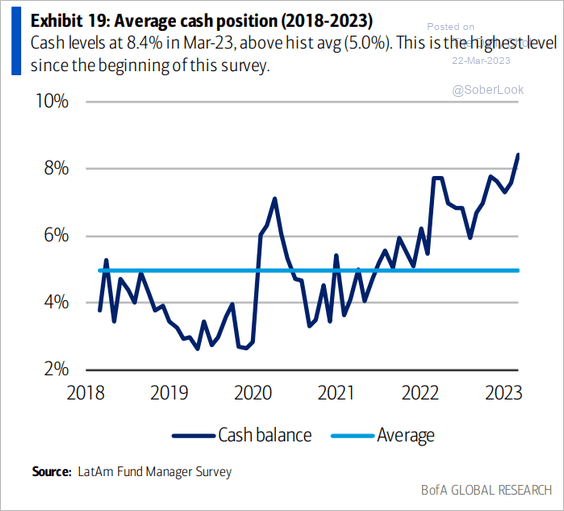

Emerging Markets: Mexican vehicle sales are rebounding.

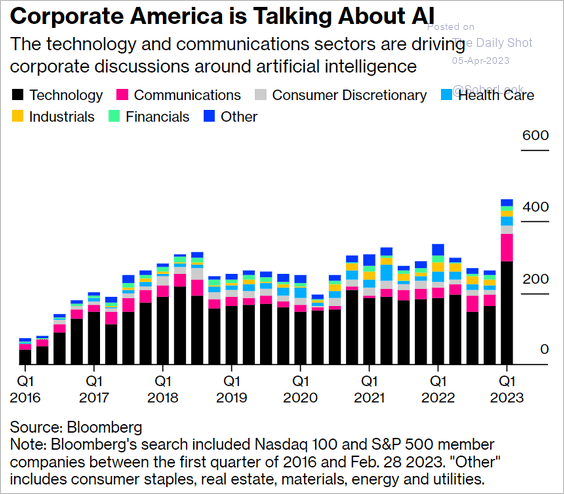

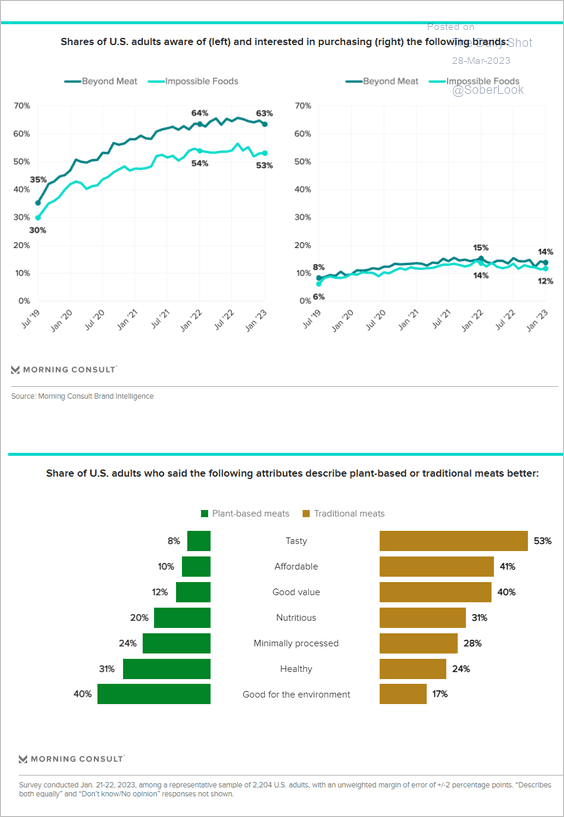

Food for Thought: Companies discussing AI:

Edited by Josh Oldmixon

Contact the Daily Shot Editor: Brief@DailyShotResearch.com

If you would like to subscribe to the full-length Daily Shot (see example), please register here.

{kind=link}