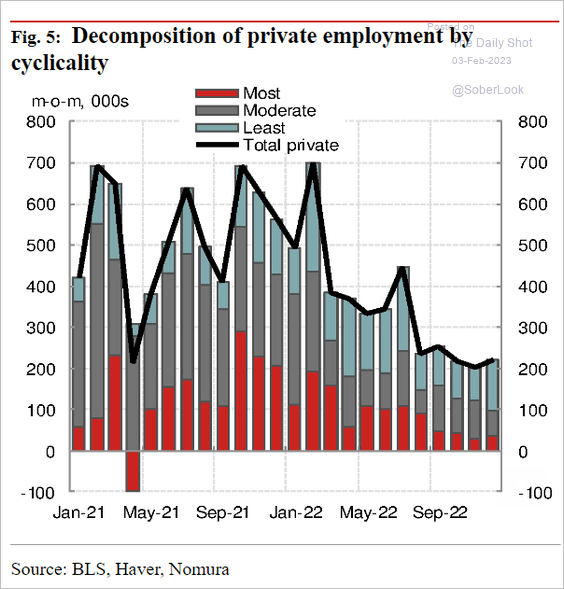

The ADP private payrolls report is signaling a hiring slowdown in January. It’s unclear if this softening will be reflected in the official jobs report.

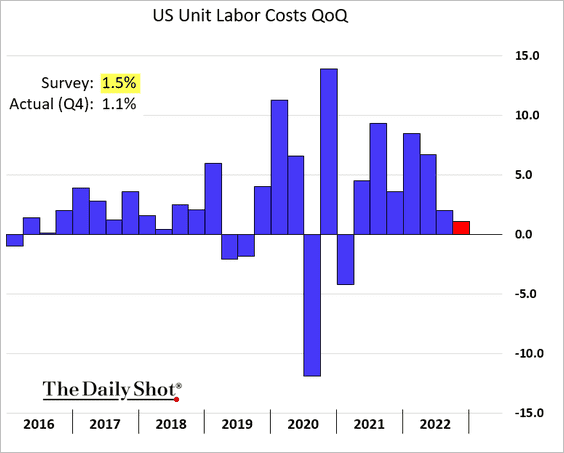

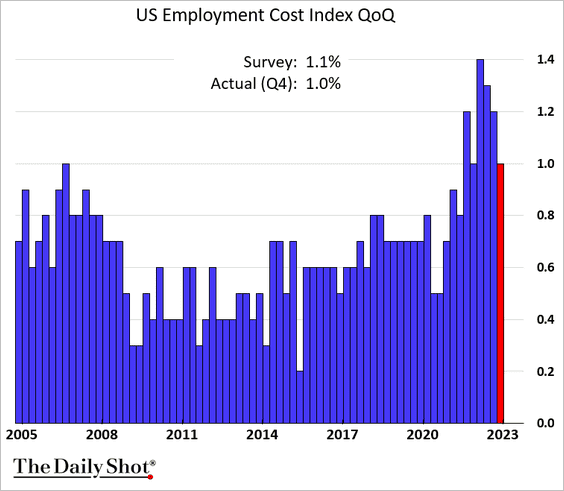

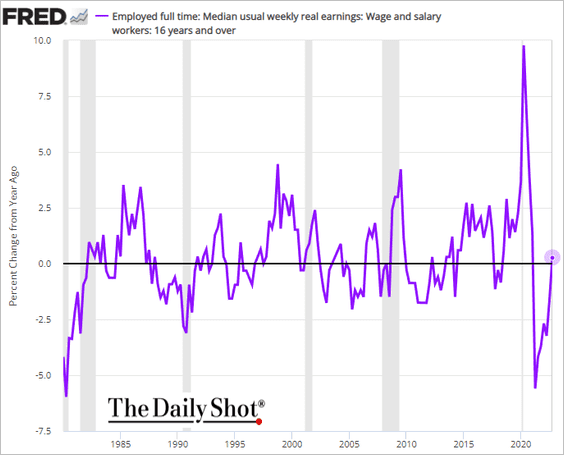

The UnitedStates: US employment cost index falls for the third quarter.

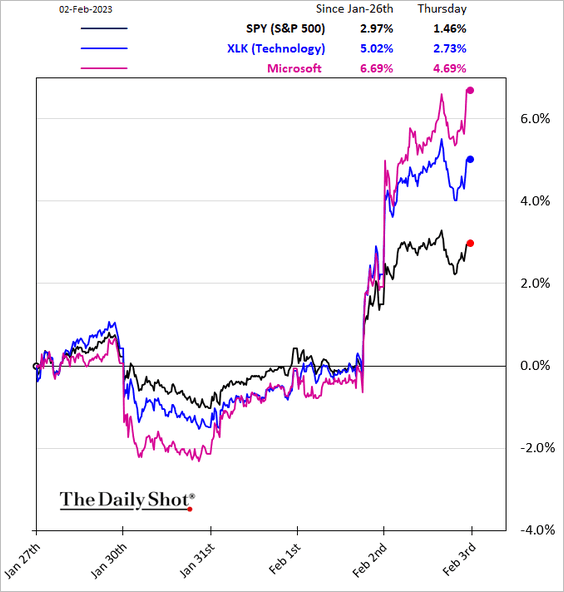

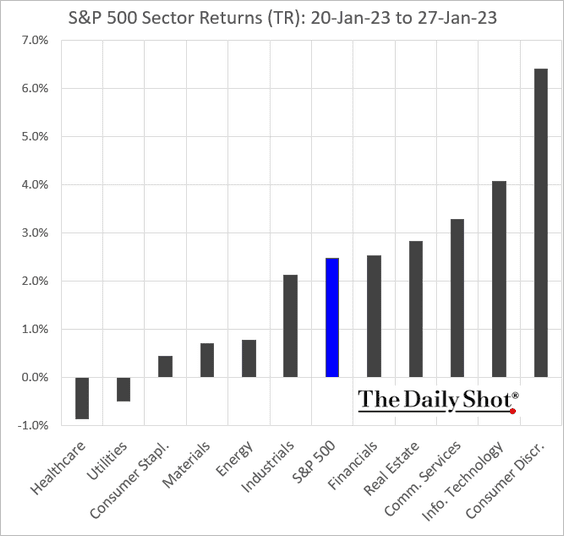

Source: The Daily Shot

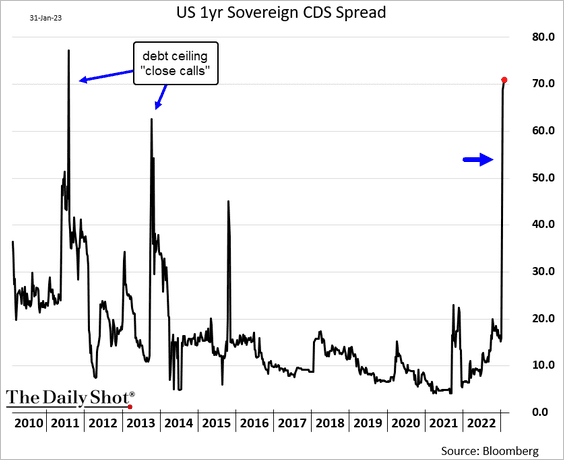

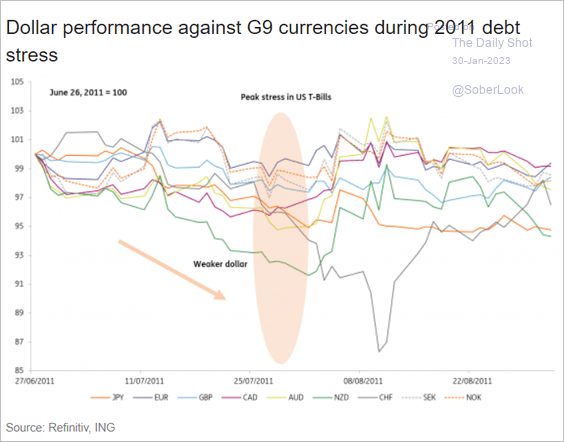

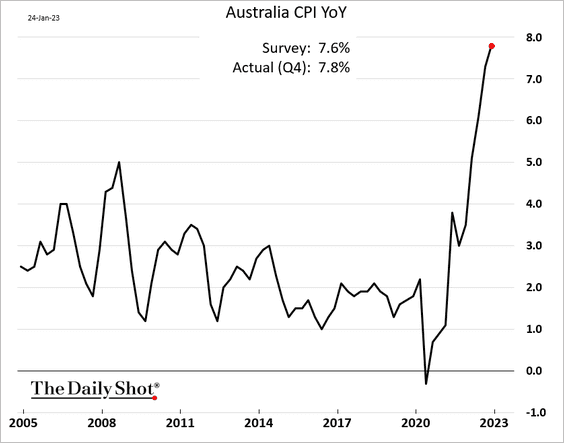

• The 1-year US sovereign credit default swap spread signals market fears similar to 2011. The market expects the government to take the debt ceiling fight to the brink.

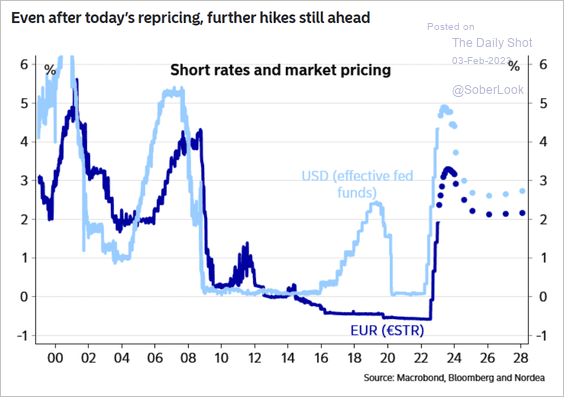

Source: Bloomberg

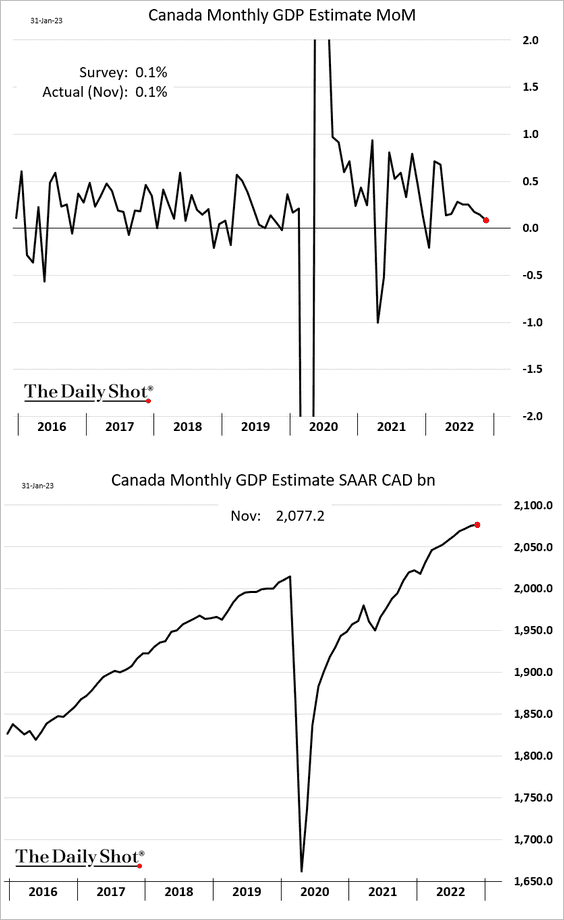

Canada: Economic growth slowed in November but remained in positive territory.

Source: The Daily Shot

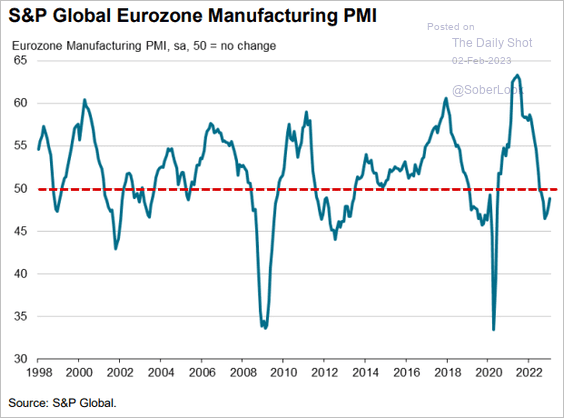

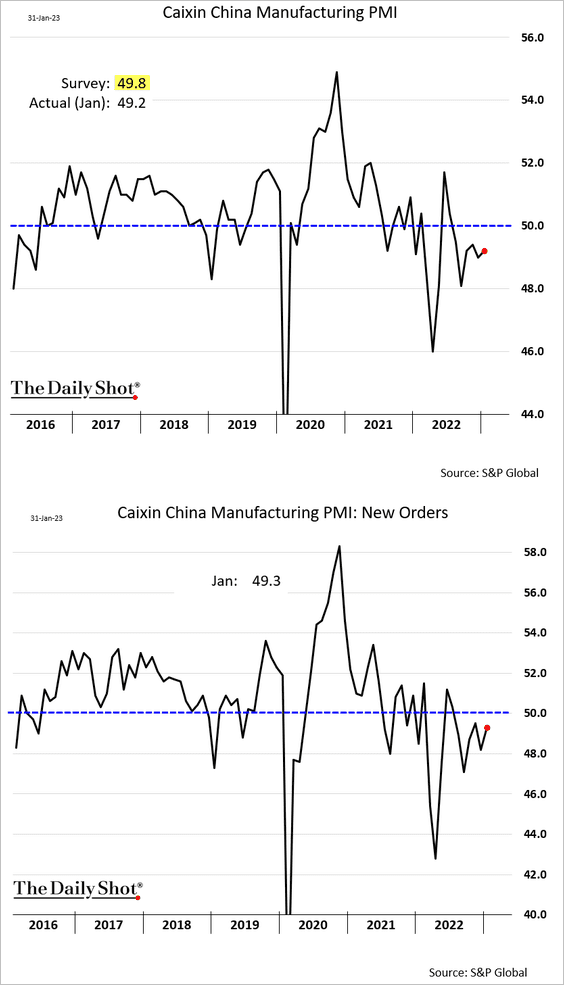

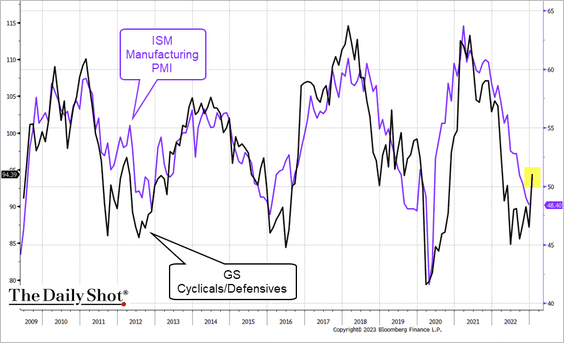

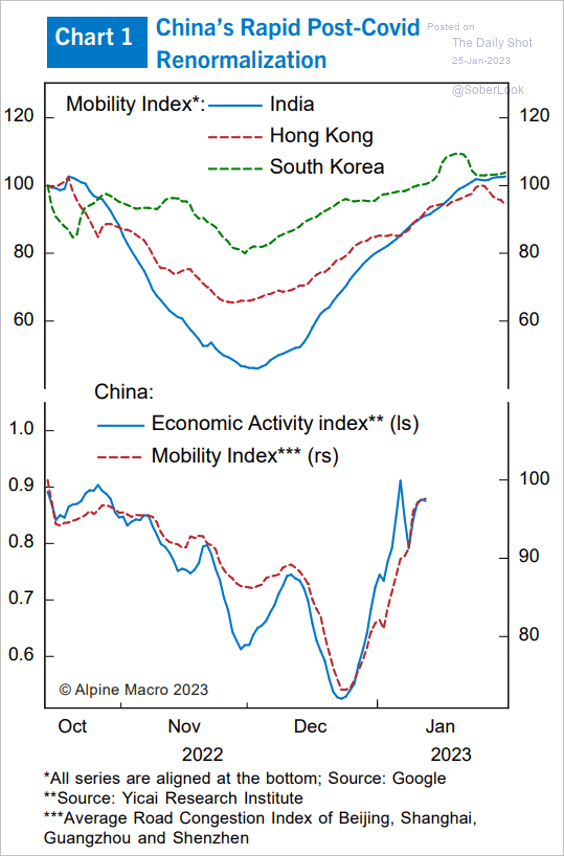

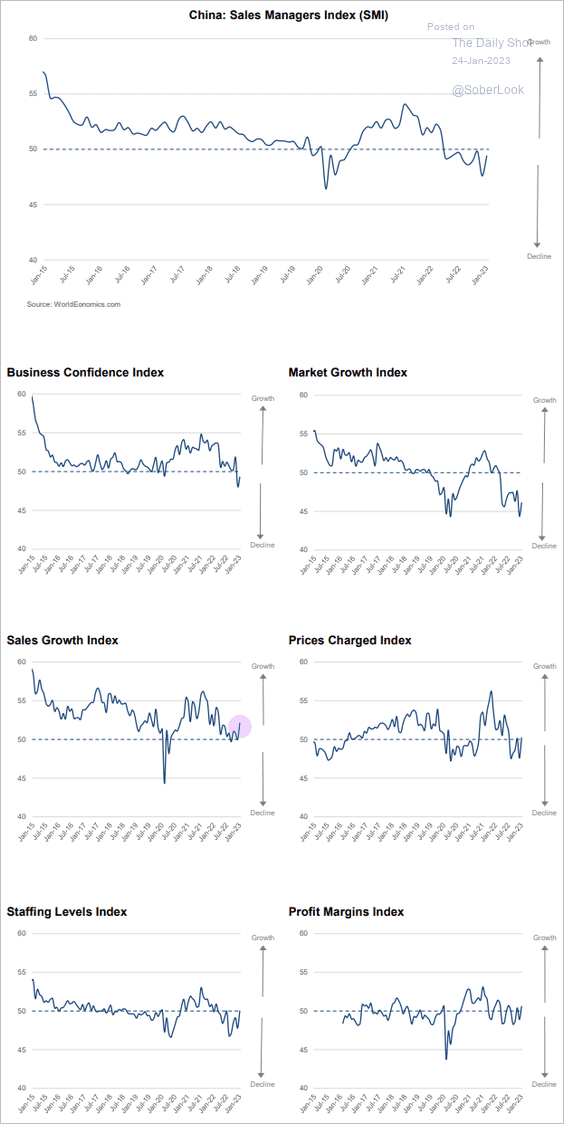

China:The manufacturing PMI data from S&P Global was less upbeat than the official report. Factory activity remains in contraction mode.

Source: The Daily Shot

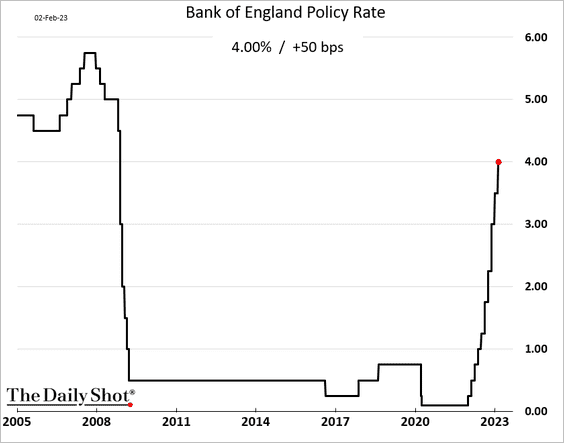

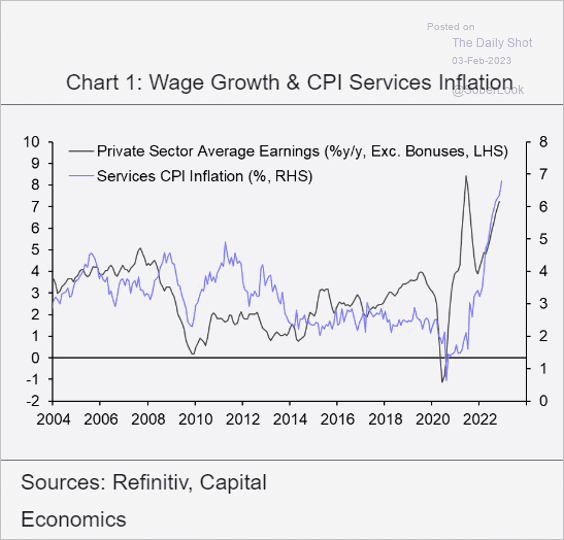

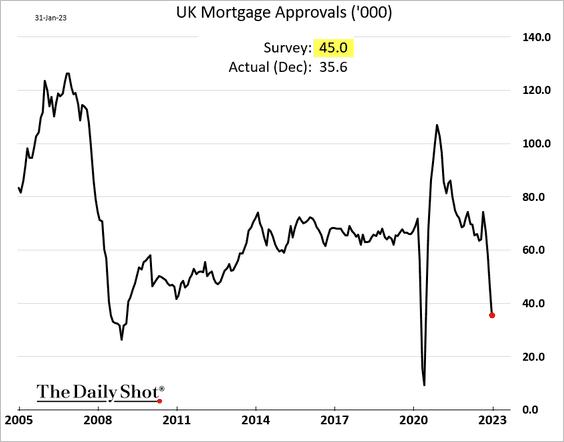

United Kingdom: Mortgage approvals in the United Kingdom fall significantly.

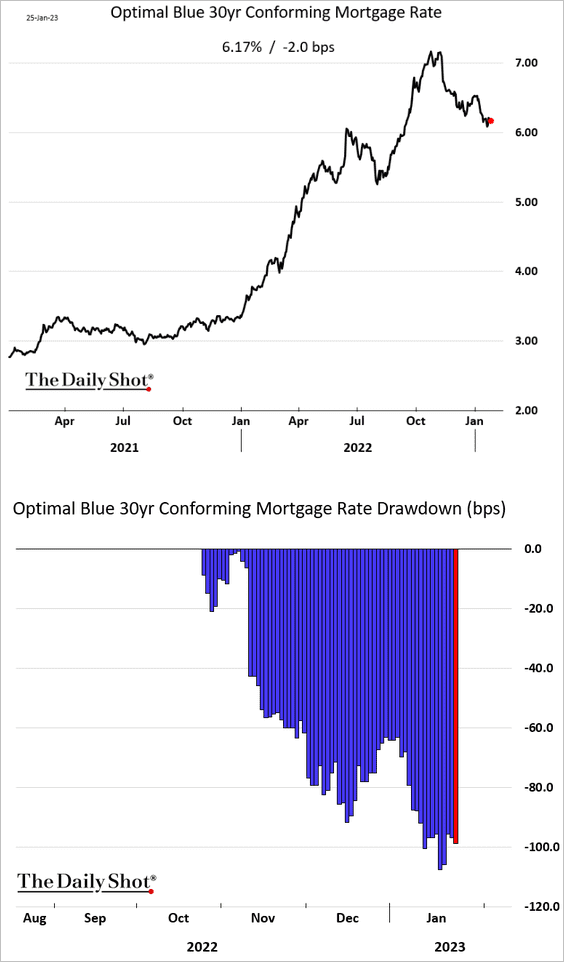

The UnitedStates: Mortgage rates are down 100 bps from the recent highs.

Source: The Daily Shot

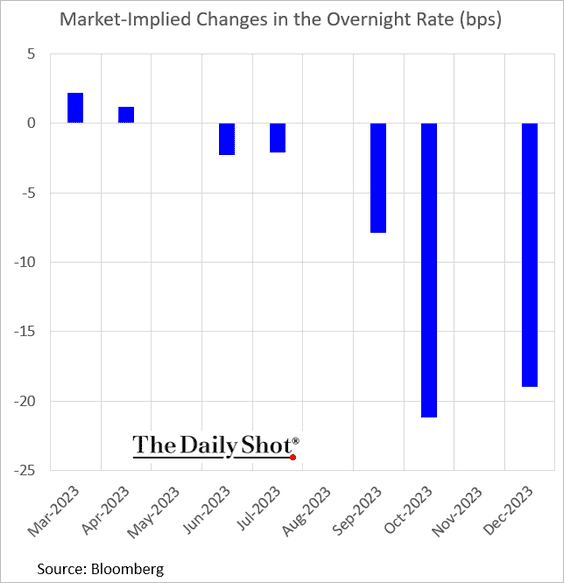

Canada: The BoC hiked rates by 25 bps and signaled a pause. The market doesn’t see any more rate increases in this cycle, with rate cuts kicking in later this year.

Source: The Daily Shot

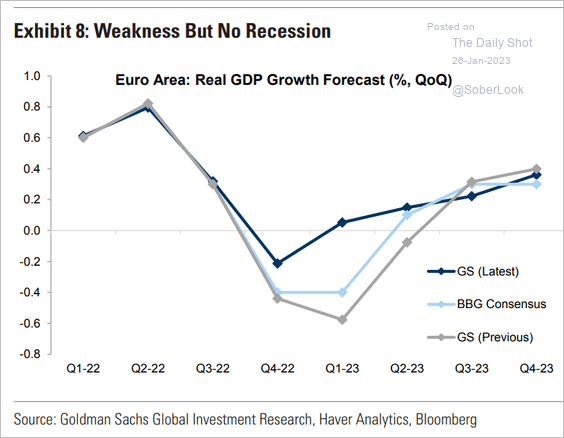

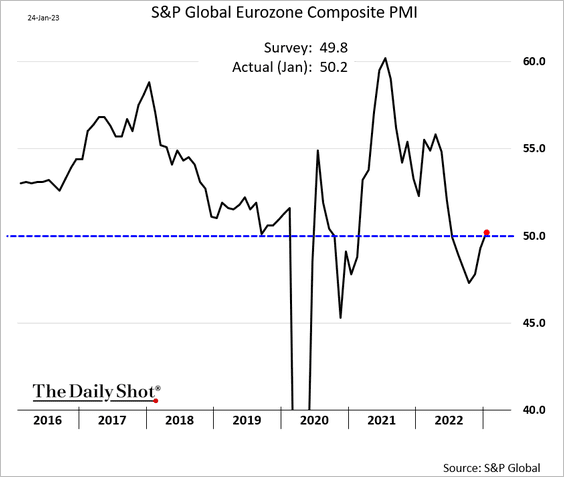

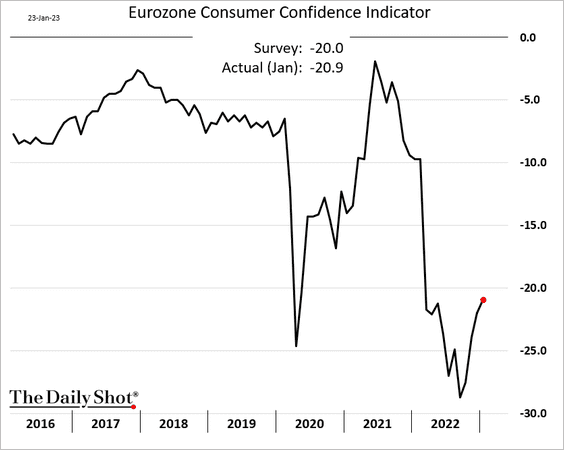

The Eurozone: Goldman no longer expects a recession in the Eurozone.

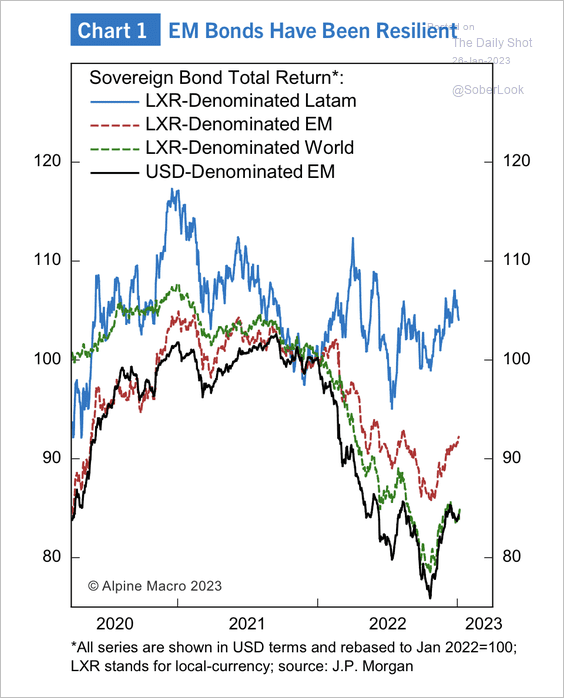

Emerging Markets: EM local currency sovereign bonds, particularly in LatAm, significantly outperformed despite a strong dollar and rising global inflation.

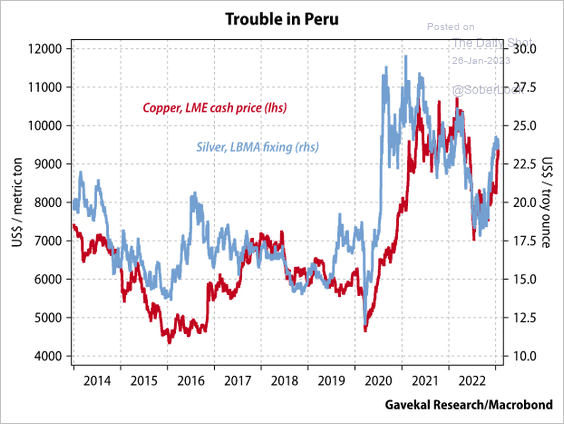

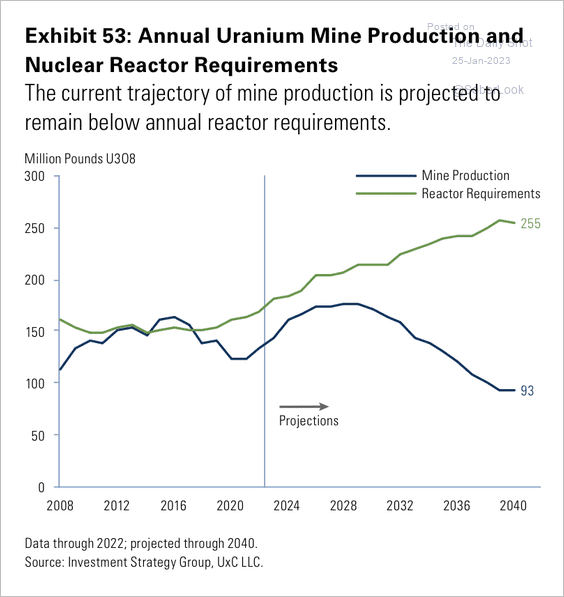

Commodities: Uranium supply has been insufficient to meet annual reactor requirements. The deficit is expected to continue over the coming years, which could raise the price of uranium.

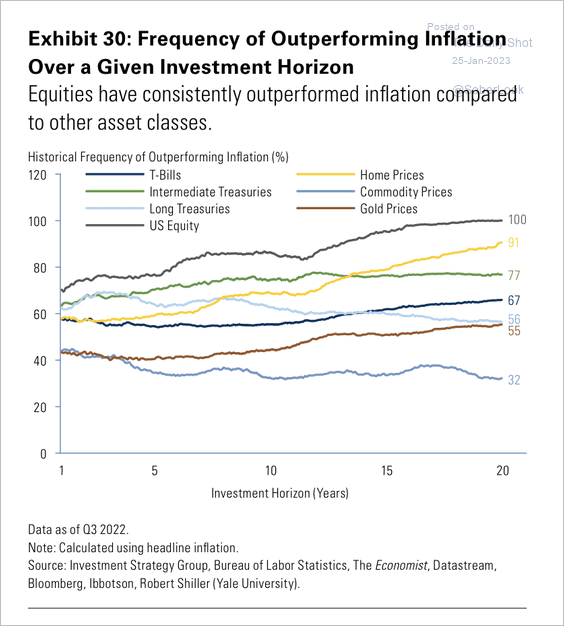

Equities: US equities have been the most effective hedge against inflation relative to other asset classes over any period between one and 20 years. According to Goldman, commodities have not been a good hedge, based on their risk/return profile in long-term portfolios.

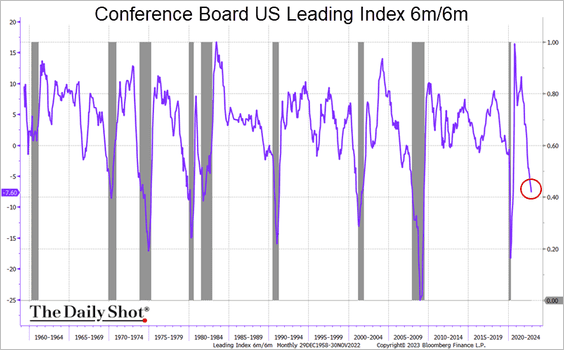

The UnitedStates: The Conference Board’s index of leading indicators has never declined this much in six months without a recession (the index goes back to the late 1950s).

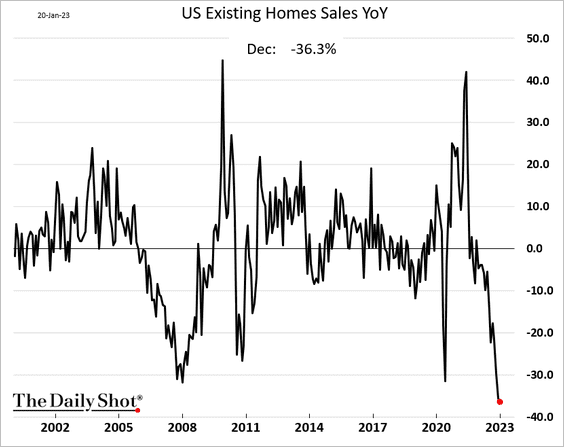

The UnitedStates: Existing home sales were very weak in December, down 36% in 2022. This is the biggest annual decline in decades.

Source: Daily Shot

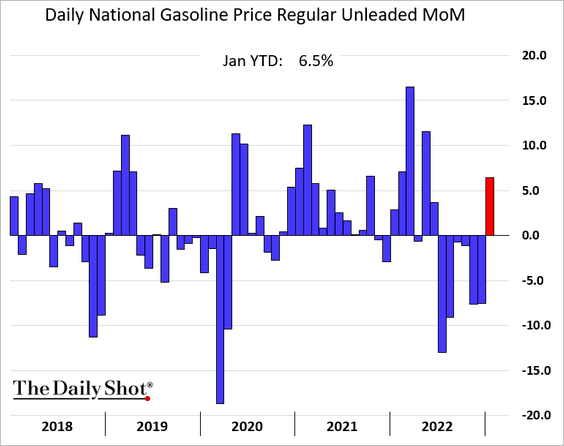

US gasoline prices are on track for their first monthly gain since last June.

Source: Daily Shot

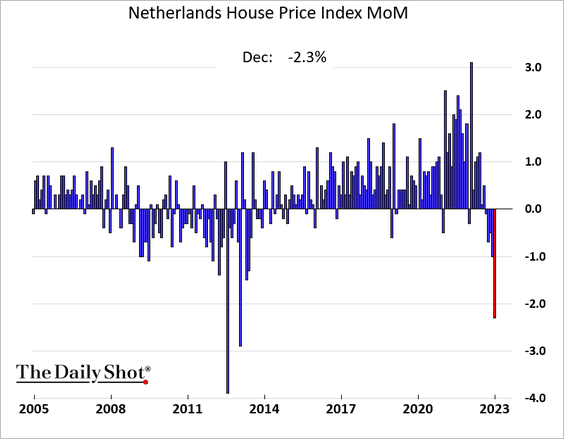

The Eurozone: Dutch home price declines have accelerated.

Source: Daily Shot

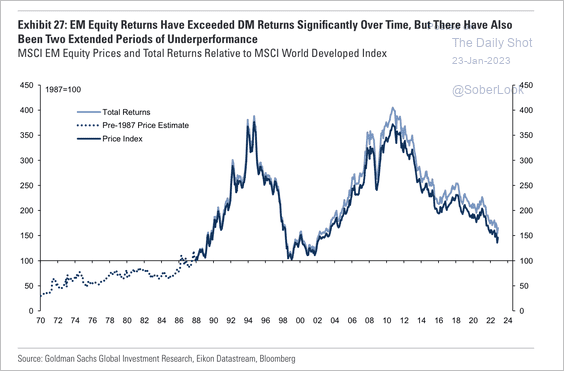

Emerging Markets: EM total equity returns have significantly underperformed developed markets in the past decade, having significantly outperformed in the previous decade.

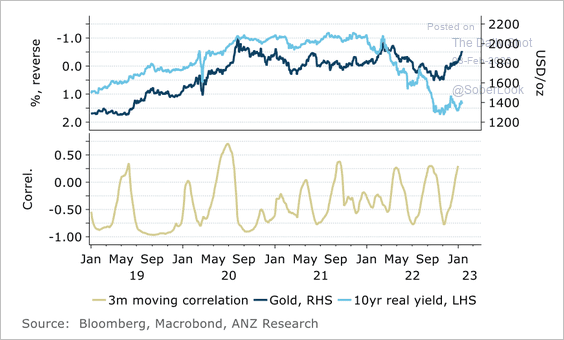

Source: The Daily Shot

Source: The Daily Shot Source:

Source:  Source: The Daily Shot

Source: The Daily Shot Source: The Daily Shot

Source: The Daily Shot

{kind=link}