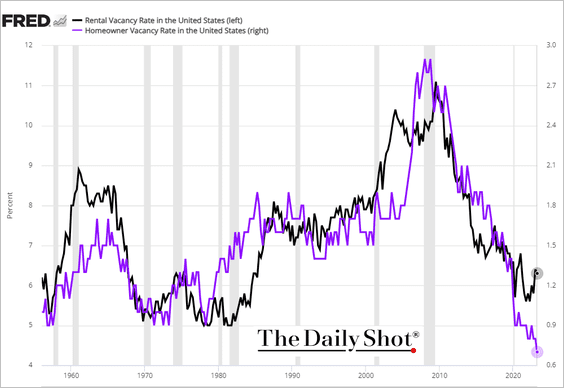

Rental vacancies are up this year, but homeowner vacancies hit a record low. The homeowner vacancy rate is defined as a proportion of homes that are for sale and vacant as a percentage of the total homeowner inventory.

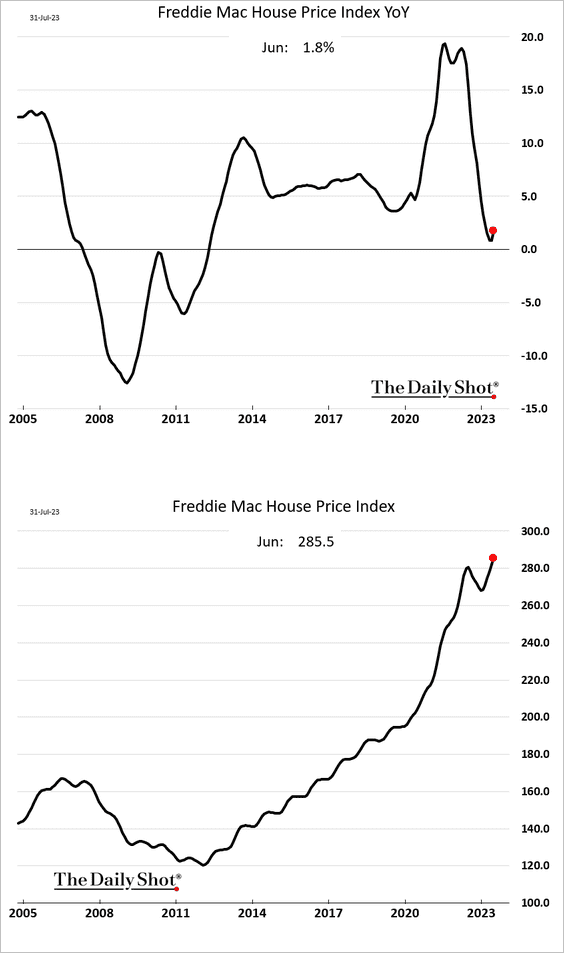

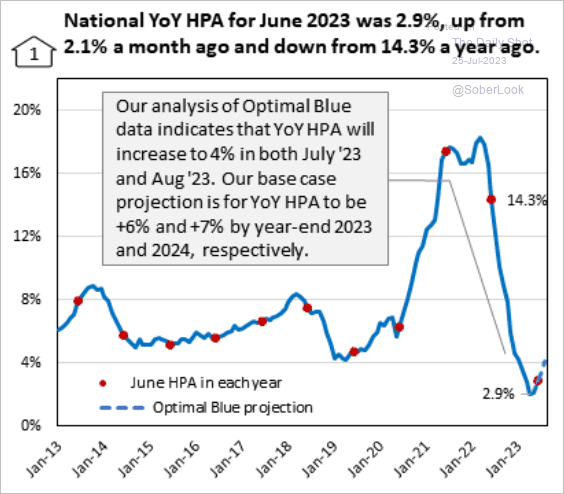

The United States: Freddie Mac’s house price index was up in June on a year-over-year basis. Note that the index didn’t cross the zero mark in this cycle.

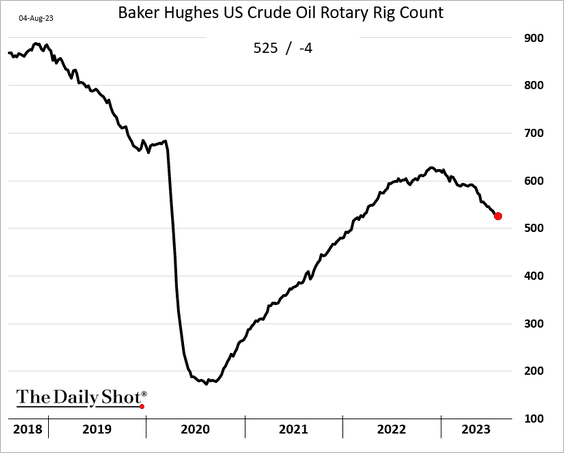

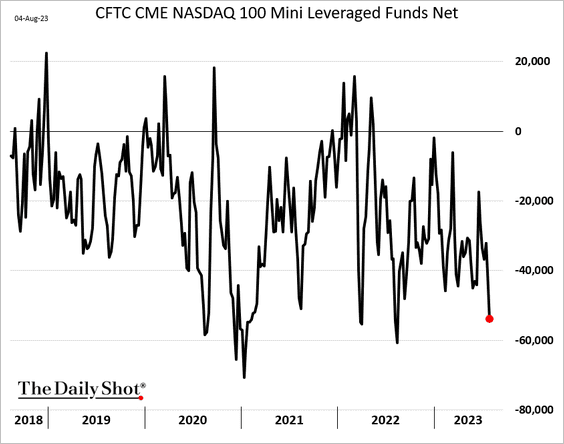

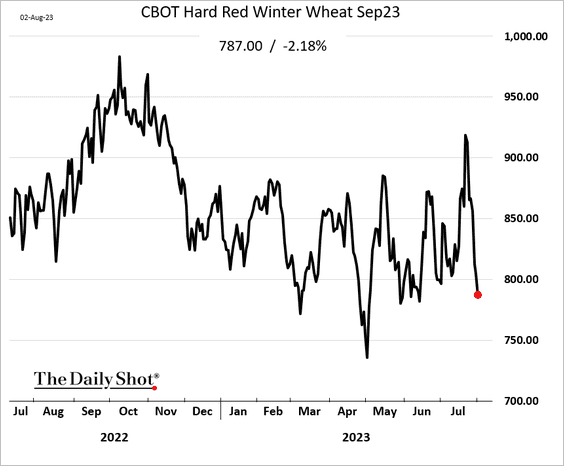

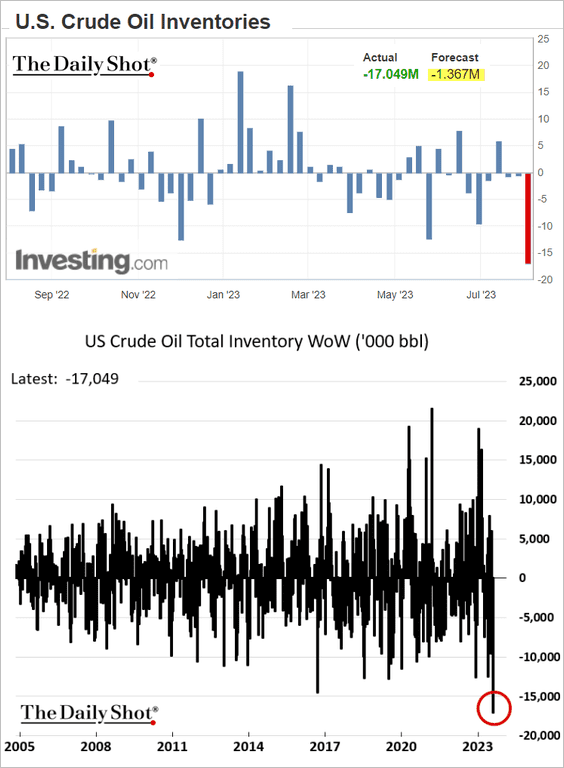

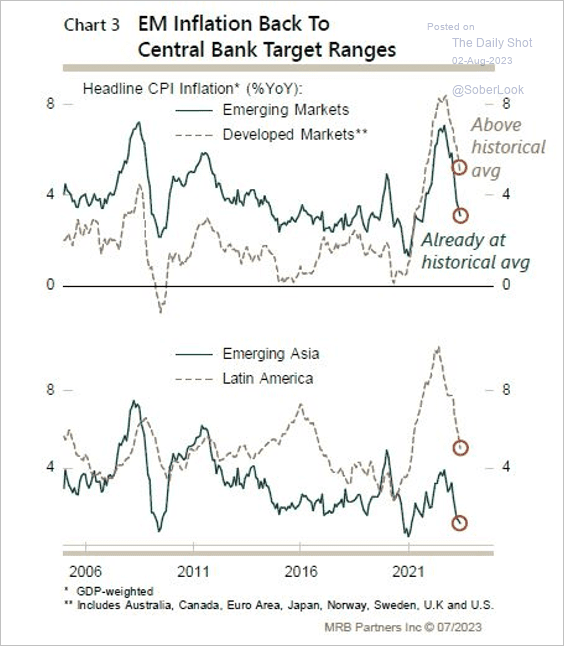

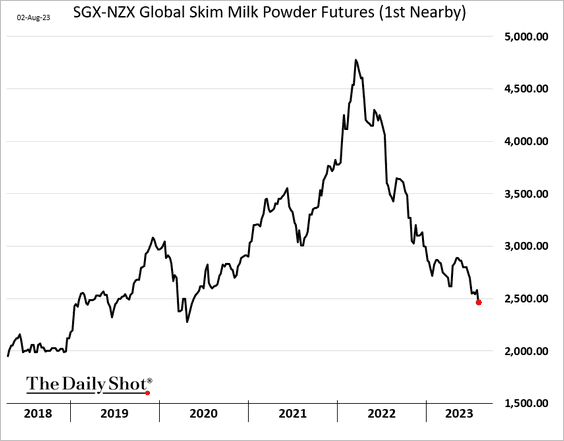

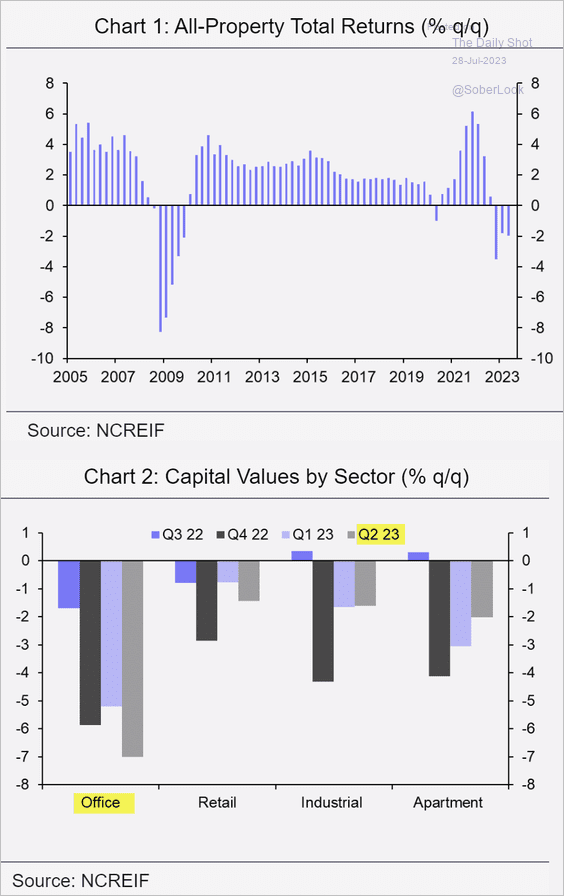

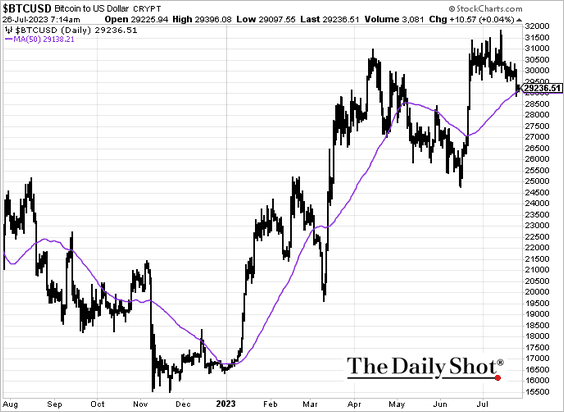

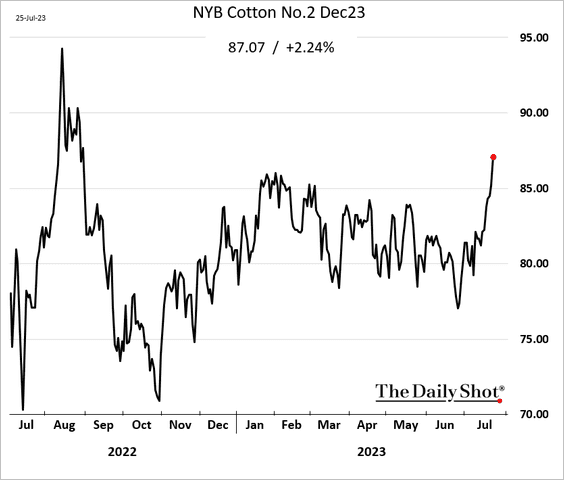

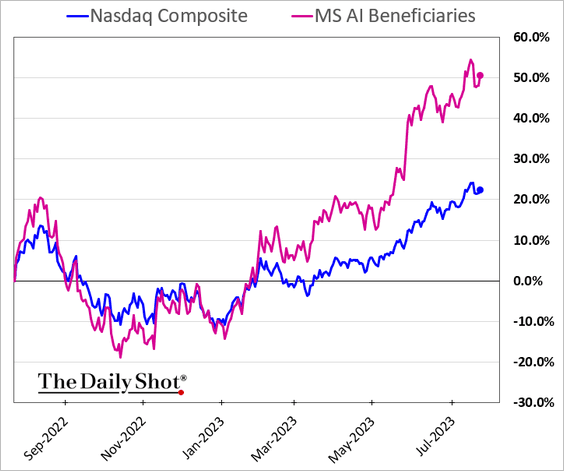

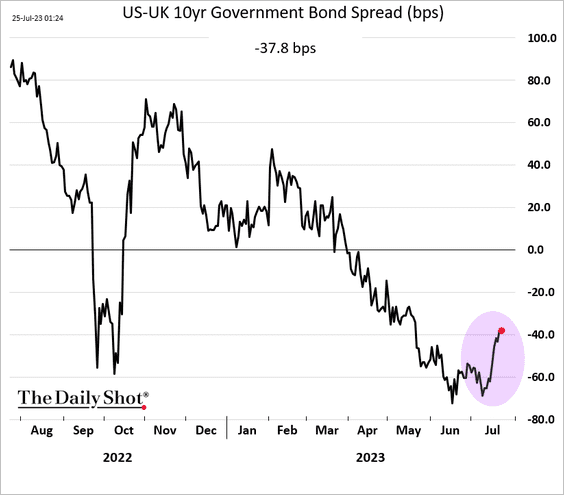

Source: The Daily Shot

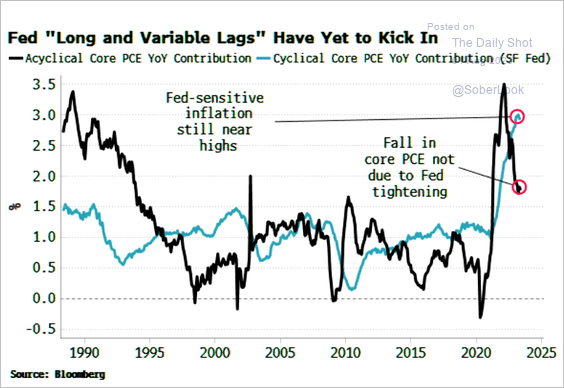

Fed rate hikes have yet to kick in. The Fed-sensitive (cyclical) CPI component is still near the highs.

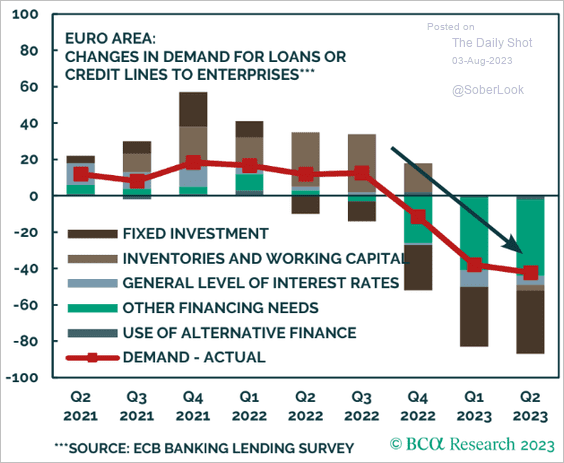

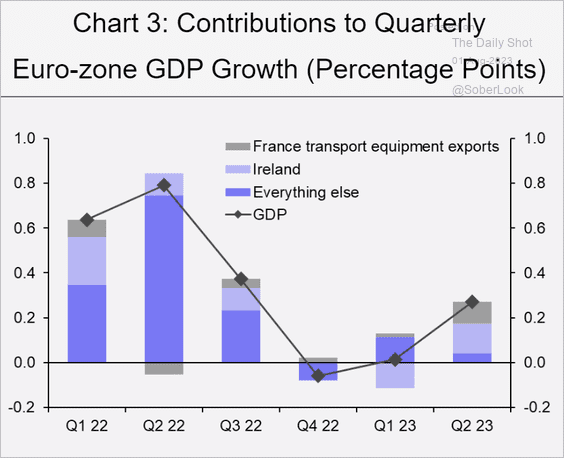

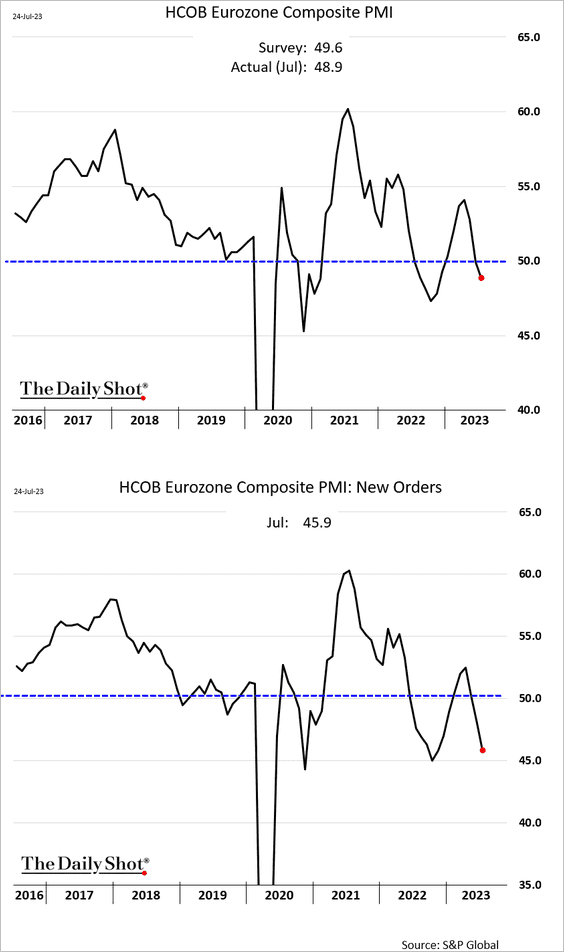

The Eurozone: The factors propelling the surge in the Euro-area’s Q2 GDP are unlikely to be sustainable. The lion’s share of these gains can be attributed to the notoriously volatile Irish GDP, which is often subject to significant revisions, and the exports of transport equipment in France, predominantly from a single cruise boat.

Before we begin, we wanted to alert you to one of our favorite weekend reads: the Weekly S&P500 ChartStorm by Callum Thomas — it features 10 handpicked charts on the US stock market covering macro, technicals, valuations, and more — it’s a quick and effective way to stay on top of the market outlook.

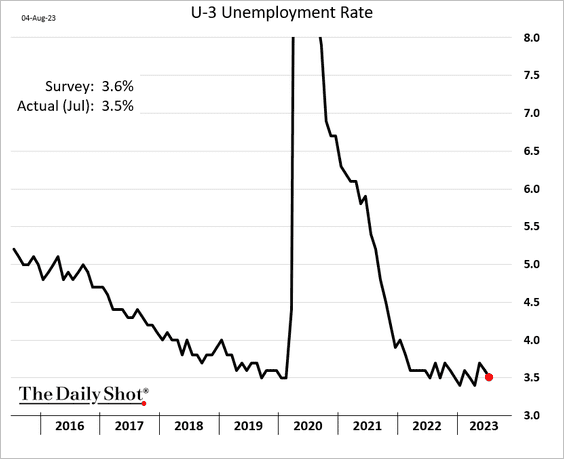

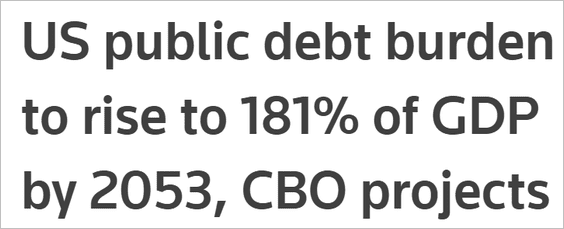

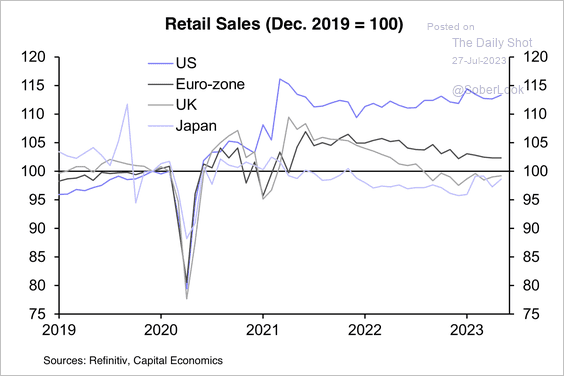

The United States: Consumer spending increased in June, with gains across goods and services.

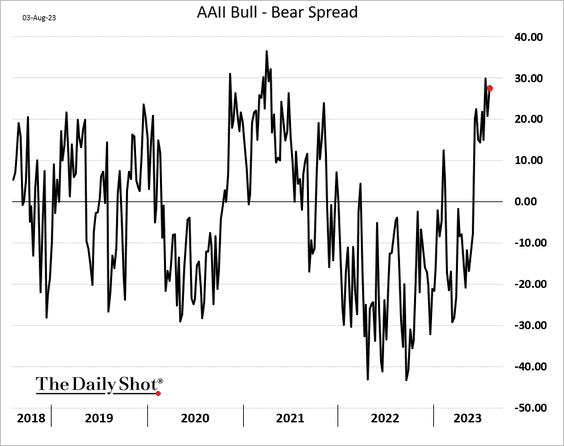

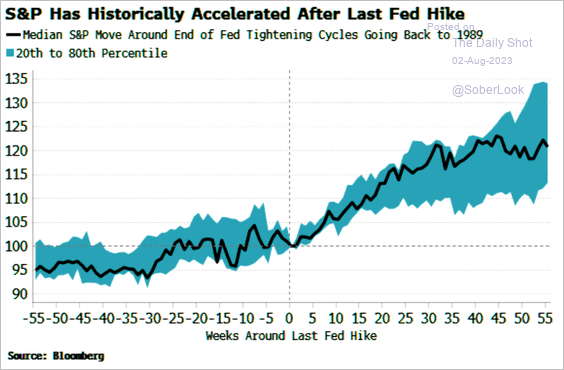

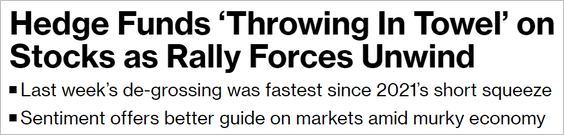

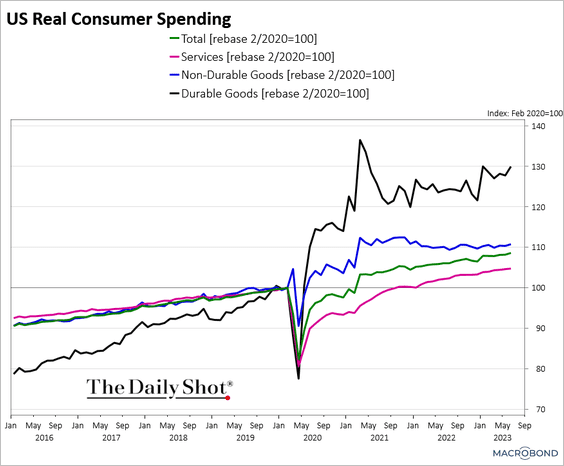

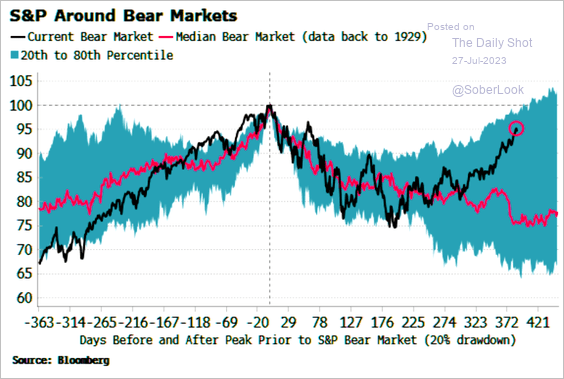

Equities: It has been a while since the S&P 500 experienced a 1%+ drop. According to SentimenTrader, this type of dynamic is almost exclusively witnessed during bull markets.

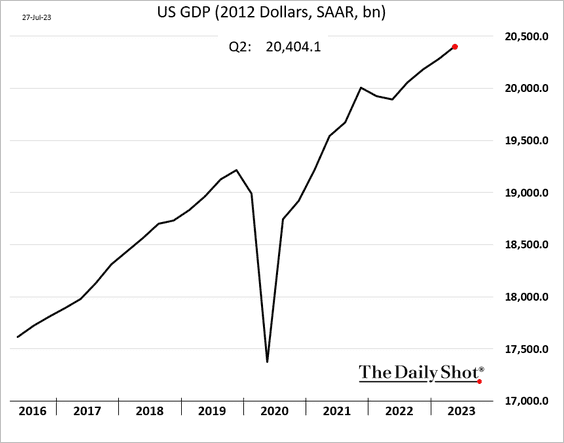

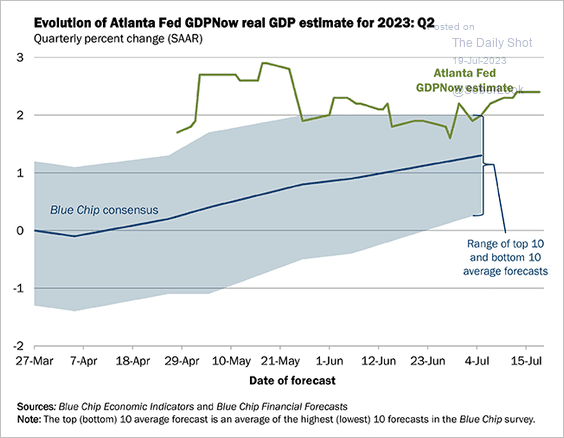

The United States: The GDP report topped expectations, signaling robust economic growth. The Atlanta Fed’s GDPNow model was much closer to the Q2 figure than the consensus forecast (see chart).

Source: The Daily ShotSource: The Daily Shot

Europe: This chart shows road freight transport between EU and non-EU countries.

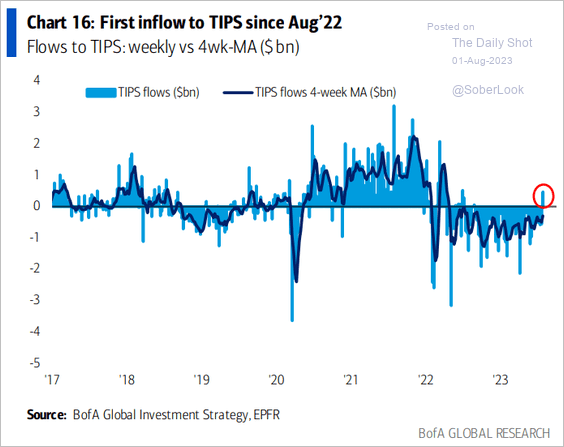

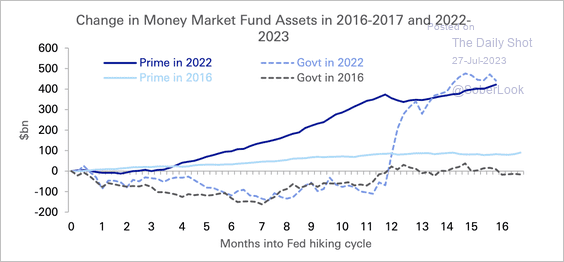

Credit: Prime money market funds experience inflows during rate hike cycles, while government funds face outflows. However, in March of this year, government money market funds became a haven for depositors.

Before we begin, we wanted to alert you to one of our favorite weekend reads: the Weekly S&P500 ChartStorm by Callum Thomas — it features 10 handpicked charts on the US stock market covering macro, technicals, valuations, and more — it’s a quick and effective way to stay on top of the market outlook.

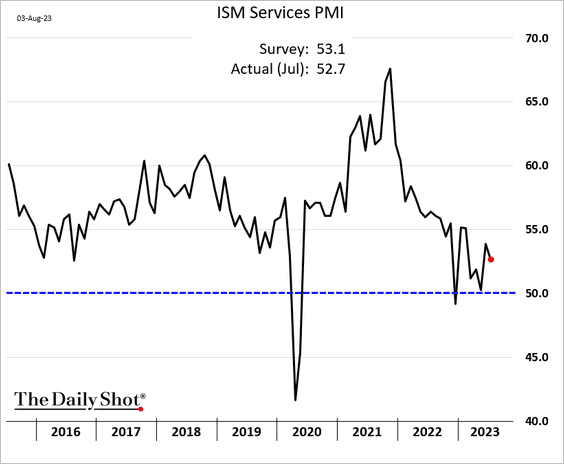

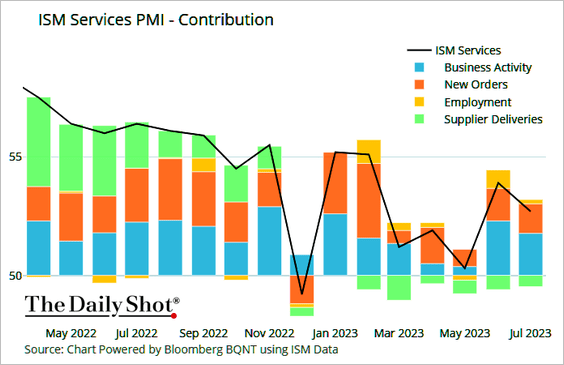

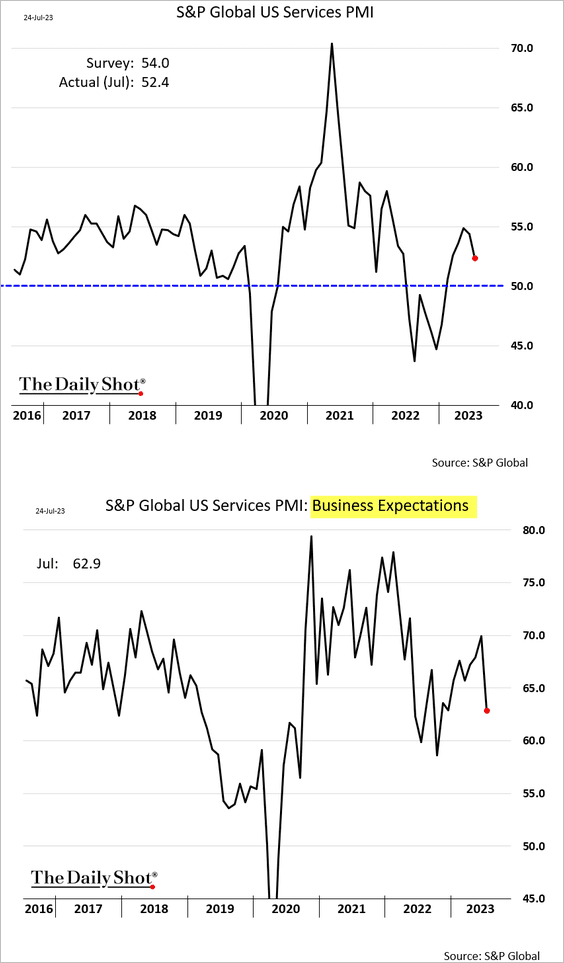

The United States: The services PMI index from S&P Global declined in July but remained in growth territory (PMI > 50). Business outlook and hiring softened.

{kind=link}